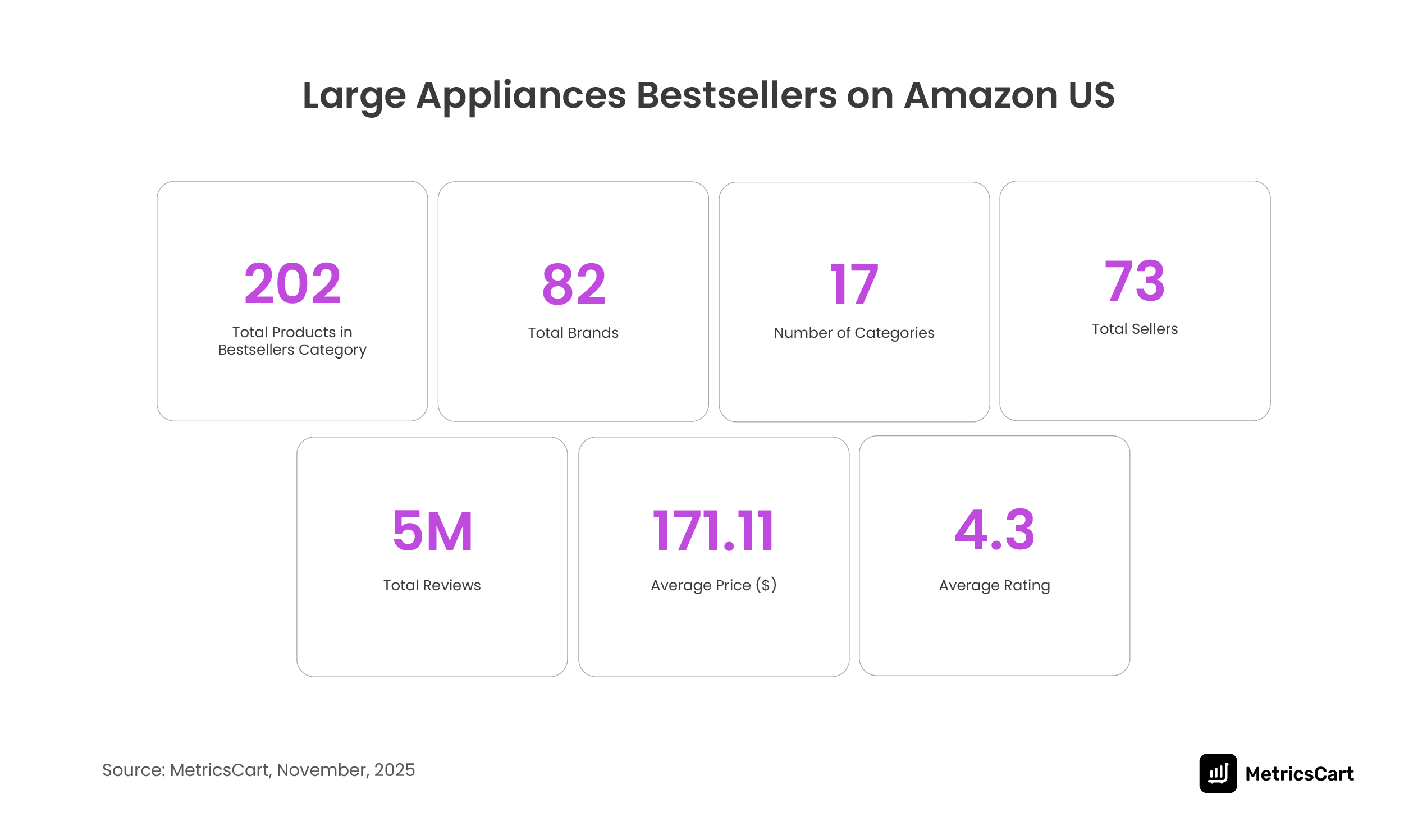

About the Report: This Digital Shelf Insights report analyzes large appliances bestsellers on Amazon between November 12 and November 26, 2025, using real-time insights from the MetricsCart digital shelf analytics platform.

It evaluates marketplace performance signals, including product rankings, category distribution, price trends, review velocity, seller activity, and brand visibility. The report is designed to help brand managers, e-commerce teams, and marketplace sellers understand how large appliances perform within Amazon’s competitive ecosystem.

Large Appliances Bestsellers on Amazon Report Highlights

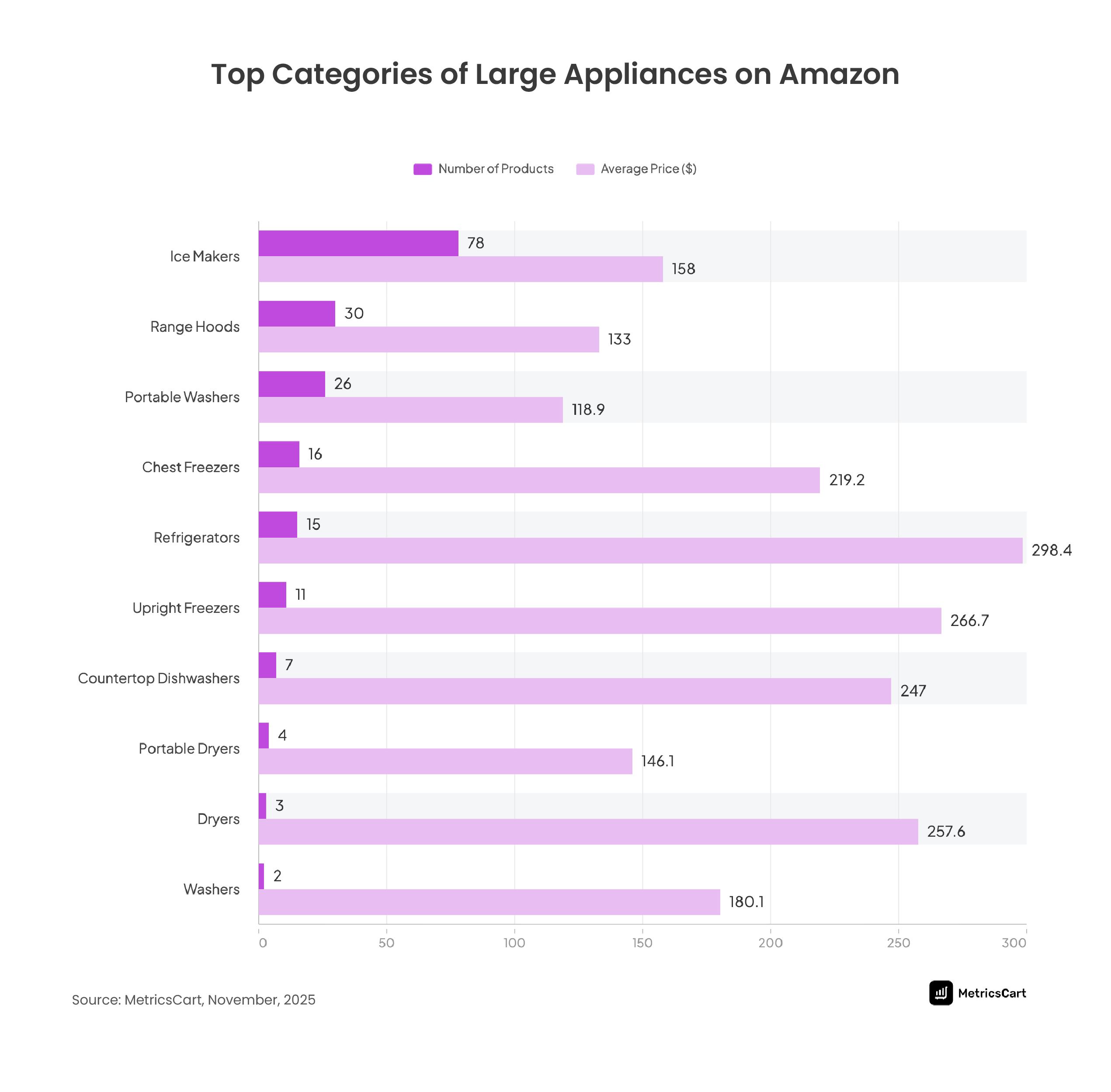

- Ice makers dominate demand with 50+ bestseller listings, making them the most competitive large appliance category on Amazon.

- Price sensitivity defines the market as top-ranked products cluster tightly between $50–$100.

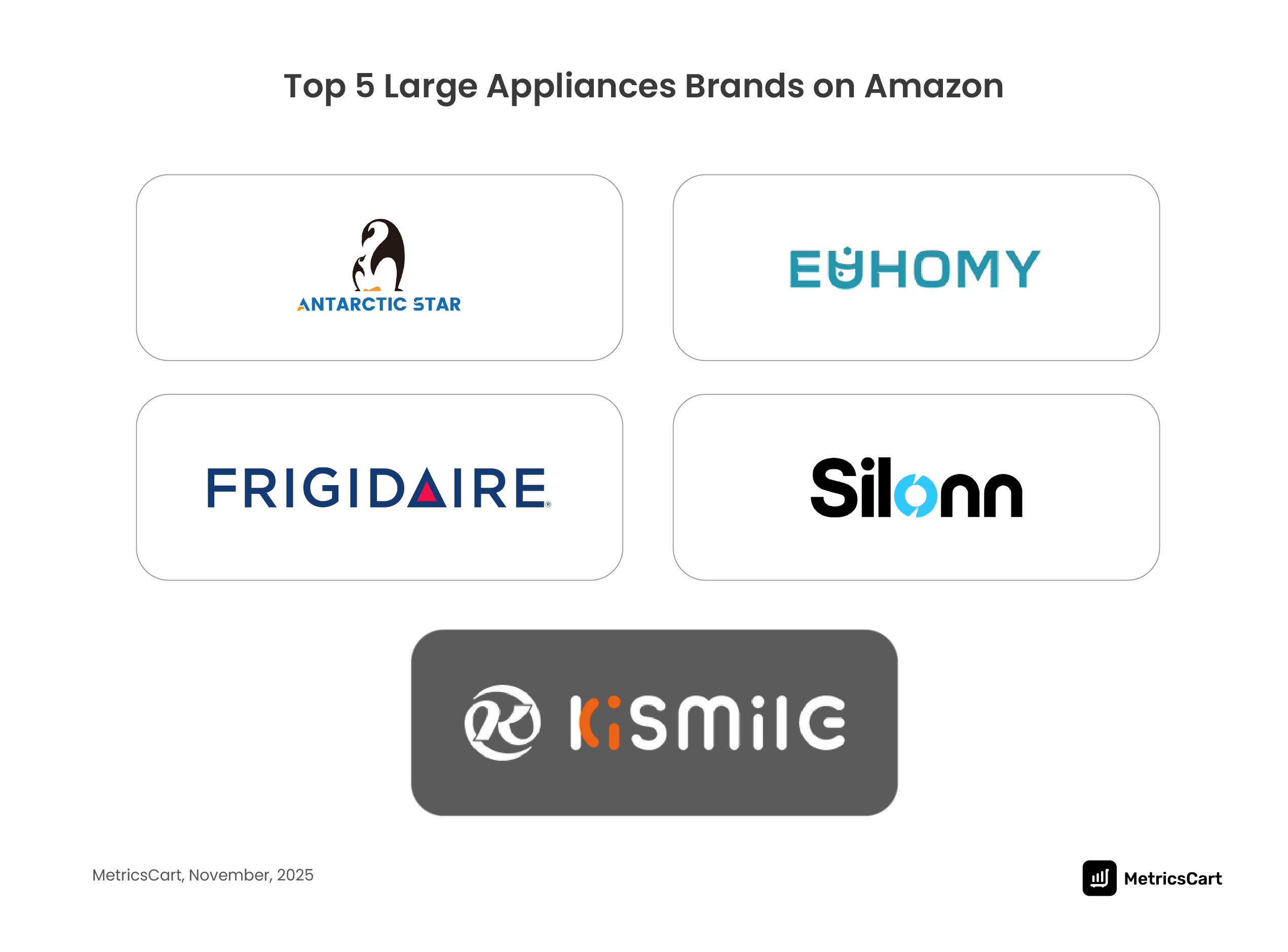

- Antarctic Star held Rank #1 for 15 consecutive days, signaling sustained demand strength and listing optimization.

- EUHOMY consistently ranked #2 and also leads in total bestseller product count.

- Catalog depth is rare, with only two brands holding more than 10 bestseller listings.

- COMFEE maintained a perfectly stable visibility with exactly five listings per day.

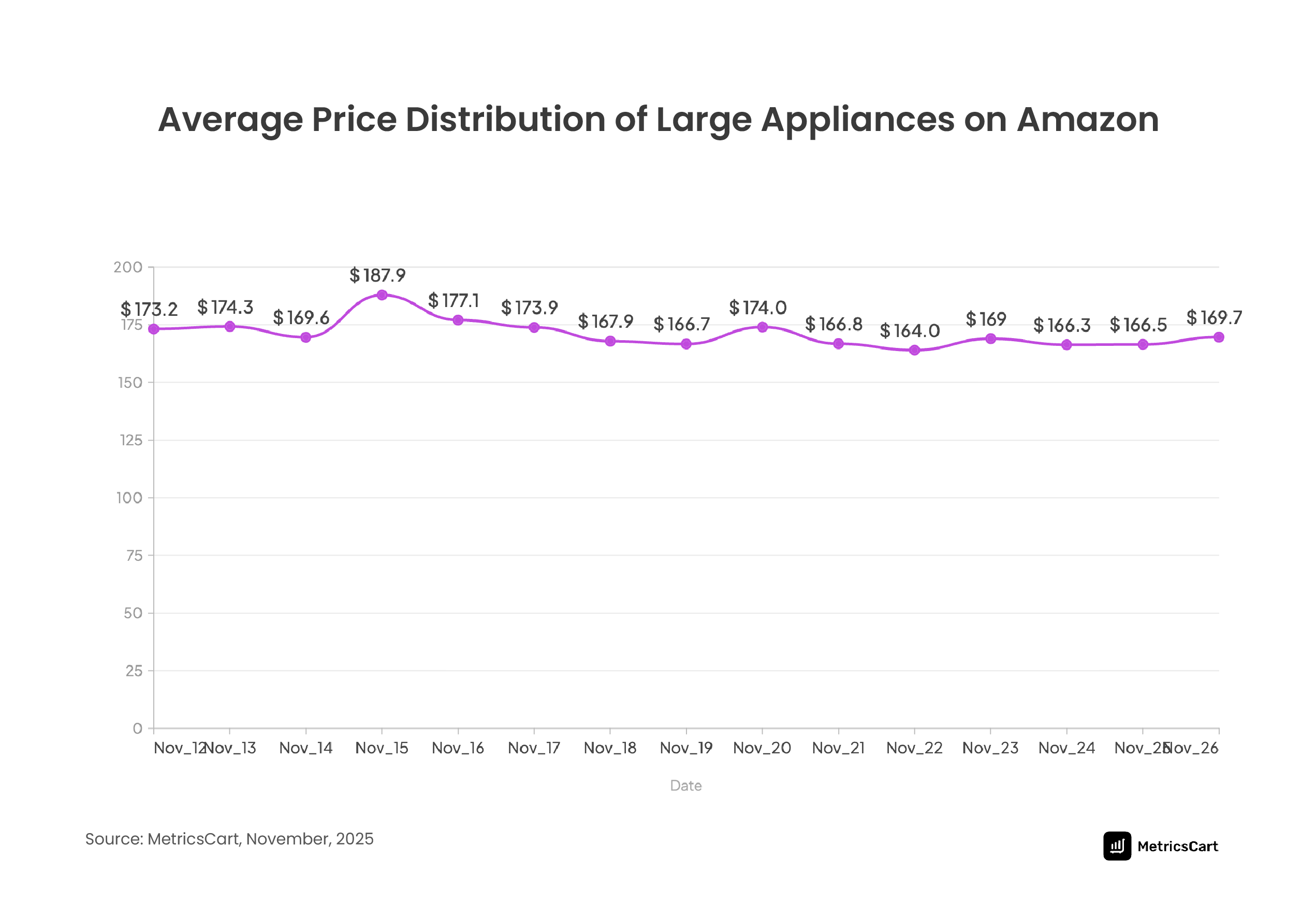

- Average bestseller prices range from $163 to $187, with noticeable short-term fluctuations rather than long-term trends.

- Premium segment leaders like GE Profile and Kenmore compete on price positioning rather than listing volume.

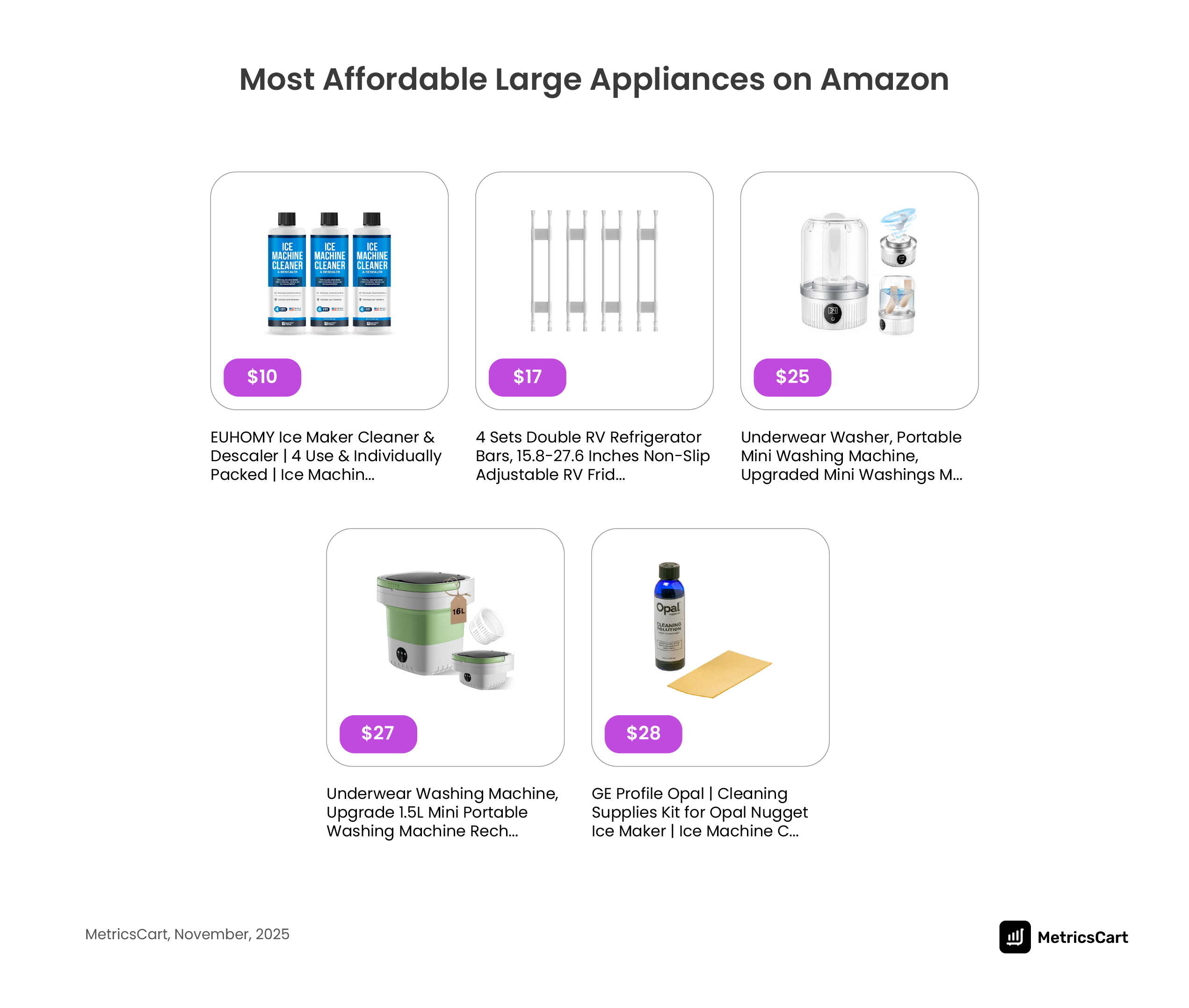

- Budget segment growth is driven by low-cost appliances priced between $10 and $47, with sellers such as HAWBATH anchoring entry-level demand.

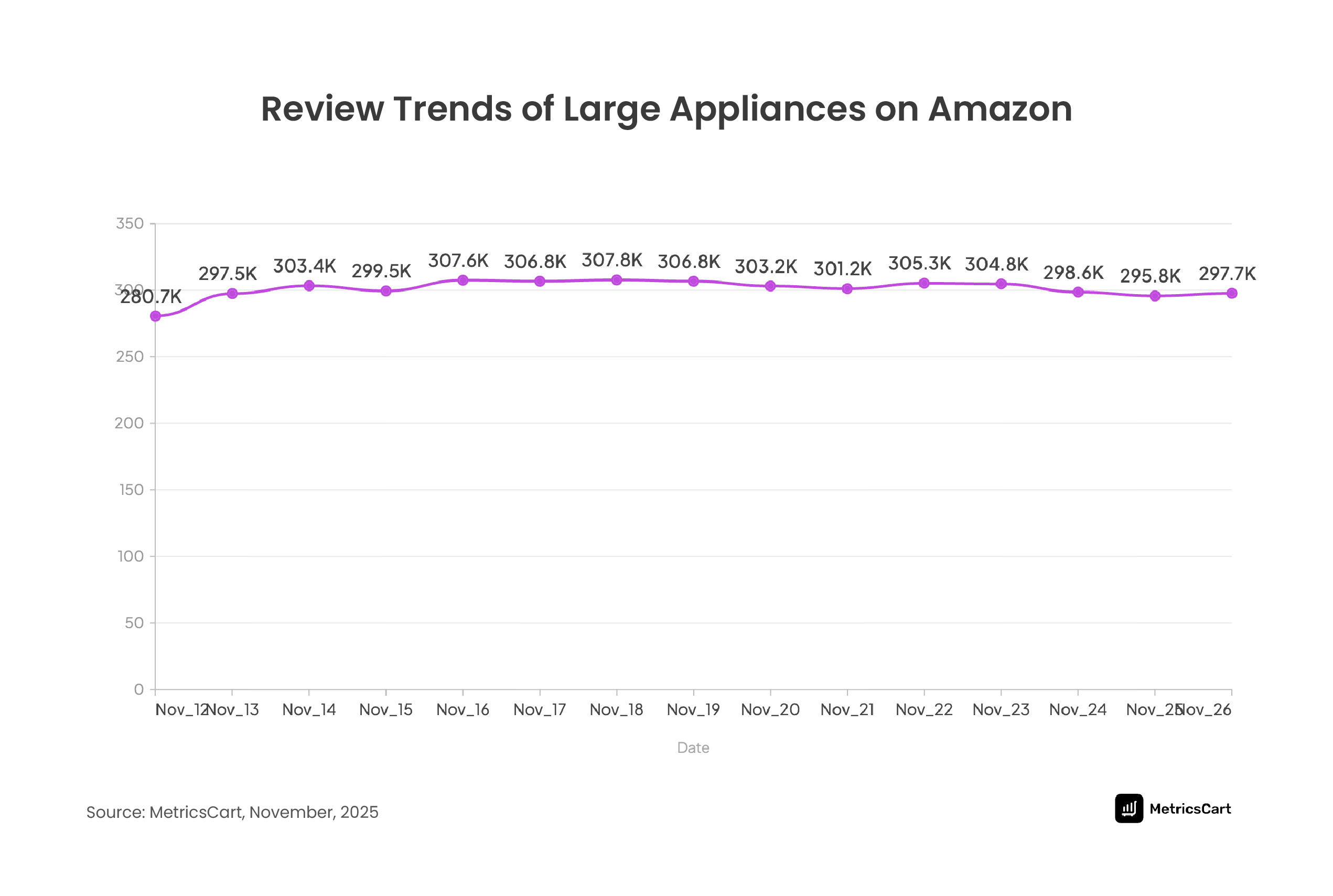

- Top-reviewed products exceed 100K reviews, indicating that review velocity strongly correlates with bestseller stability.

- Mid-tier brands maintain steady visibility, including Frigidaire and Silonn, showing consistent but not dominant performance.

Introduction

Large appliances, also known as white goods or major appliances, are essential household machines that are heavy, high-investment, and built to last. These products primarily fall into two categories: kitchen and laundry equipment. Common items include refrigerators, freezers, ovens, ranges, dishwashers, washing machines, dryers, and air conditioners.

Traditionally, these appliances were purchased in physical stores. However, with the rise of e-commerce, an increasing share of sales is now happening online.

Online sales of large appliances have steadily grown, driven by the convenience of home delivery, access to detailed product reviews, and the ability to easily compare prices. According to Statista, online sales are expected to account for 28.4% of total revenue in the Household Appliances market by 2026.

And among e-commerce platforms, Amazon, with a 37.6% market share of US online sales, plays a crucial role in this growth. With 86-90 million daily visits and around 149 orders per second, Amazon not only dominates the marketplace but also influences pricing behavior, consumer expectations, and category trends.

Taken together, these macro trends explain why analyzing large appliances bestsellers on Amazon provides valuable insight into real consumer demand. Bestseller data serves as a real-time indicator of pricing elasticity, category momentum, and competitive positioning, allowing brands and marketplace teams to understand not just what is selling but why it is winning.

Category Performance Analysis: Which Large Appliances Dominate Amazon Bestsellers

The bestseller landscape for large appliances on Amazon is not evenly distributed across product types. Instead, demand is highly concentrated in a few specific categories, revealing clear patterns in consumer purchasing behavior and marketplace competition.

Ice Makers: The Coolest Players in the Market

Among all categories analyzed, ice makers dominate the bestseller rankings, accounting for more than 50 products during the study period.

In the MetricsCart analysis, this dominance appears as a much taller bar than all other appliance types, signaling significantly higher listing frequency and sales velocity.

This indicates that consumer demand within large appliances is currently skewed toward compact, specialized appliances rather than traditional full-size units.

Portable Washers: The Underdog Appliances Gaining Steam

Following ice makers, range hoods, and portable washers form the second tier of demand, each exceeding 25 listings. This could be because consumers shopping online for large appliances prefer products that are easier to install, ship, and use without professional setup.

Refrigerators: Chilled to Perfection

At the opposite end of the spectrum, refrigerators represent the most expensive category, but with only about 15 bestseller listings.

This highlights a key marketplace dynamic: higher-priced appliances have lower ranking density because they sell in lower volumes despite higher revenue per unit.

The category pricing reinforces this trend. Lower-priced categories cluster tightly within narrow price bands, indicating intense competition and price sensitivity. Higher-priced categories show wider price dispersion, reflecting brand differentiation, feature variation, and lower direct price competition.

The category pricing reinforces this trend. Lower-priced categories cluster tightly within narrow price bands, indicating intense competition and price sensitivity. Higher-priced categories show wider price dispersion, reflecting brand differentiation, feature variation, and lower direct price competition.

These patterns reveal a structural shift in online appliance purchasing. Consumers are far more likely to buy smaller, portable, or niche appliances online, while larger, high-installation products still face friction in e-commerce environments. In practical terms, the bestseller ecosystem rewards categories that combine moderate pricing, easy shipping, and immediate usability.

From a strategic standpoint, category selection is as important as product optimization. Brands entering high-velocity categories gain faster visibility and ranking potential, while those competing in slower categories must rely more heavily on pricing strategy, reviews, and differentiation to maintain placement.

Brand Performance & Competitive Landscape: Leaders, Stable Players, and Volatile Competitors

The Amazon large appliances bestseller ecosystem is not controlled by a single dominant brand. Instead, it operates as a layered competitive structure in which leadership, stability, and volatility shape brand positioning.

At the top of the rankings, Antarctic Star demonstrates clear dominance, holding the #1 bestseller position for 15 consecutive days. This consistent top placement typically reflects a strong combination of competitive pricing, conversion efficiency, and steady demand.

Right behind it, EUHOMY maintains a persistent #2 position, forming a stable duopoly at the top of the market. Such stability suggests these brands have optimized their listings, pricing, and inventory in ways that consistently align with Amazon’s ranking signals.

A second tier of brands competes for visibility without achieving dominance. Companies such as Frigidaire, Silonn, Kismile, and Igloo rotate through mid-rank positions, each fluctuating between positions #3 and #5. This pattern indicates strong competition where small changes in price, reviews, or conversion rates can shift rankings quickly.

Consistency, however, is not only about top positions. COMFEE stands out for maintaining exactly five bestseller listings every day during the analysis period. In the listing presence chart, this appears as a perfectly flat line, signaling exceptional stability. This kind of consistency often reflects disciplined catalog strategy, inventory control, and optimized product pages.

Mid-tier steady performers such as BLACK+DECKER, Midea, and Sndoas show moderate but reliable visibility, typically maintaining between two and four listings daily.

In contrast, brands like Goavelife, ecozy, and AMZCHEF exhibit high volatility. Their visibility shows frequent rises and drops in listing count, a pattern often associated with competitive pressure, inconsistent demand, or reliance on short-term promotional boosts.

Another notable competitive factor is catalog depth. Only two brands hold more than 10 bestseller listings, confirming that broad product portfolios are rare and therefore strategically valuable. Brands with larger catalogs occupy more digital shelf space, increasing their probability of ranking success across multiple positions.

Overall, the competitive landscape shows that Amazon’s large appliances category rewards consistency more than legacy brand recognition. Sustained ranking performance is driven by pricing alignment, review accumulation, and listing optimization rather than brand size alone. For marketplace competitors, visibility is not inherited. It is engineered daily.

Pricing Intelligence & Elasticity Trends: How Price Positioning Shapes Bestseller Rankings

Pricing plays a decisive role in determining which products appear among large appliances bestsellers on Amazon. Most top-ranked listings cluster within a narrow $50–$100 price band, revealing a highly price-sensitive market where small price differences can significantly influence conversions and rankings. This concentration shows that high performers are rarely the cheapest or most expensive options but instead sit near the perceived value sweet spot.

Across categories, average bestseller prices range from $163 to $187, though trend graphs show frequent short-term fluctuations rather than steady movement. A clear decline between November 16–22 illustrates how temporary promotions or competitive repricing can quickly shift rankings on the Amazon appliances best-sellers list.

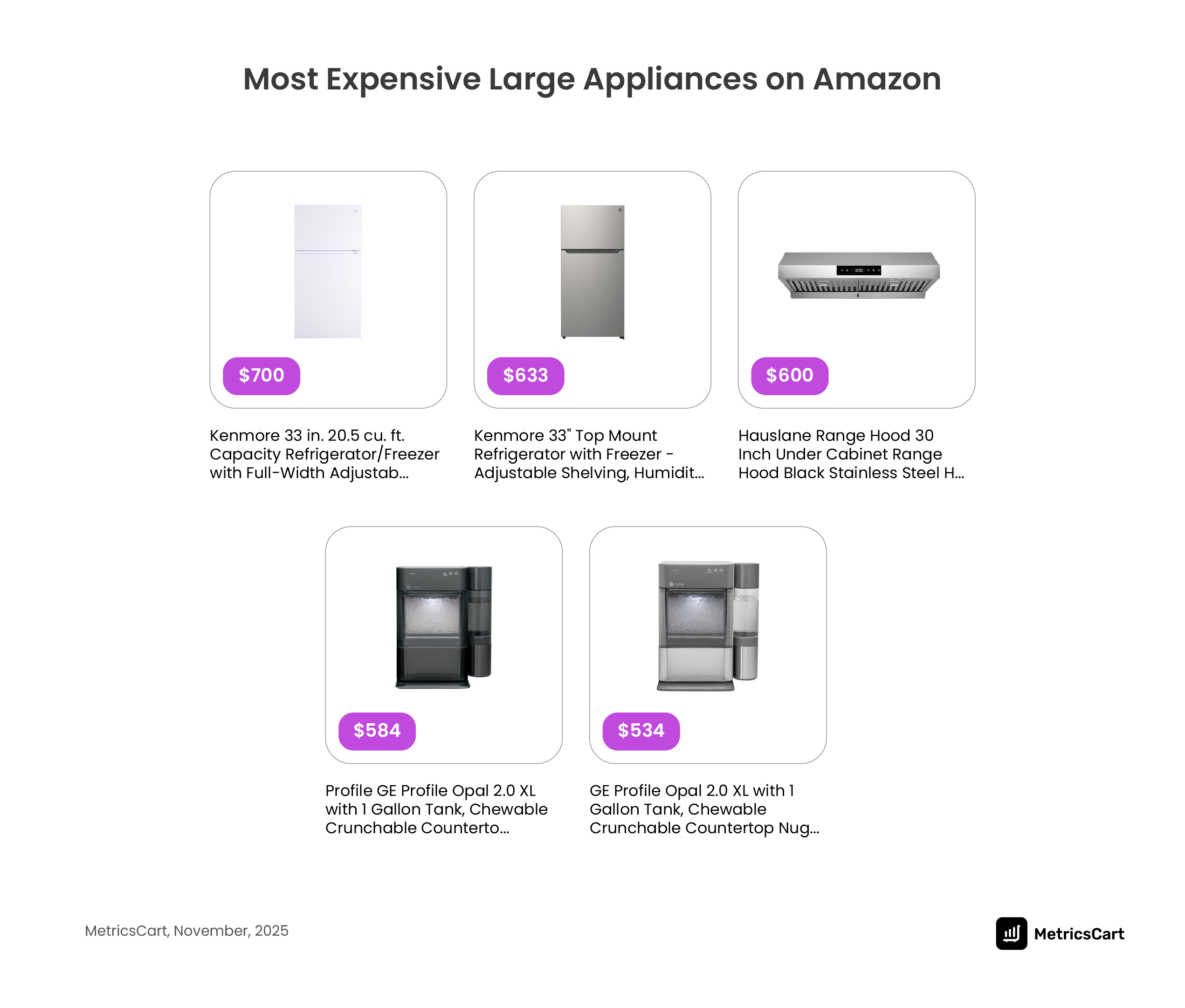

Distinct pricing tiers also separate premium and budget strategies. High-end brands like GE Profile and Kenmore operate in higher brackets with fewer listings, reflecting margin-focused positioning. Meanwhile, entry-level products priced at $10–$47 from sellers such as HAWBATH rely on affordability to gain visibility among Amazon’s best-selling large appliances in 2025.

Seller comparisons reinforce this pattern. Listings sold directly by Amazon average about $196, while premium sellers like BANGSON average roughly $353.

The takeaway is simple: success is driven not by the lowest price, but by the right price.

READ MORE | Price Matching on Amazon vs. Walmart: What Every Brand and Seller Should Know

Review & Demand Signals Behind Large Appliances Bestsellers on Amazon

Customer reviews play a decisive role in determining which products appear on the list of best-selling large appliances on Amazon. MetricsCart insights reveal the top-performing listings consistently exceed 100,000 reviews while maintaining average ratings near 4 stars, showing that sustained demand—not temporary spikes—drives visibility on the Amazon appliances best sellers list.

Review trends show counts remaining tightly clustered between 303K and 308K from November 17–22, indicating steady purchasing activity. Earlier in the period, totals jumped from roughly 280.7K to 303.4K, reflecting a surge in conversions often triggered by pricing or visibility changes common among Amazon best selling large appliances in 2025.

Products with higher review volume also experience less ranking volatility, confirming that review equity stabilizes performance. Brands such as EUHOMY and Frigidaire demonstrate this pattern, reinforcing that strong review momentum is a key driver of visibility for both premium and best-budget large appliances on Amazon.

READ MORE | Beyond Transactions: How Shopper Behavior Analysis Drives Smarter Retail Decisions

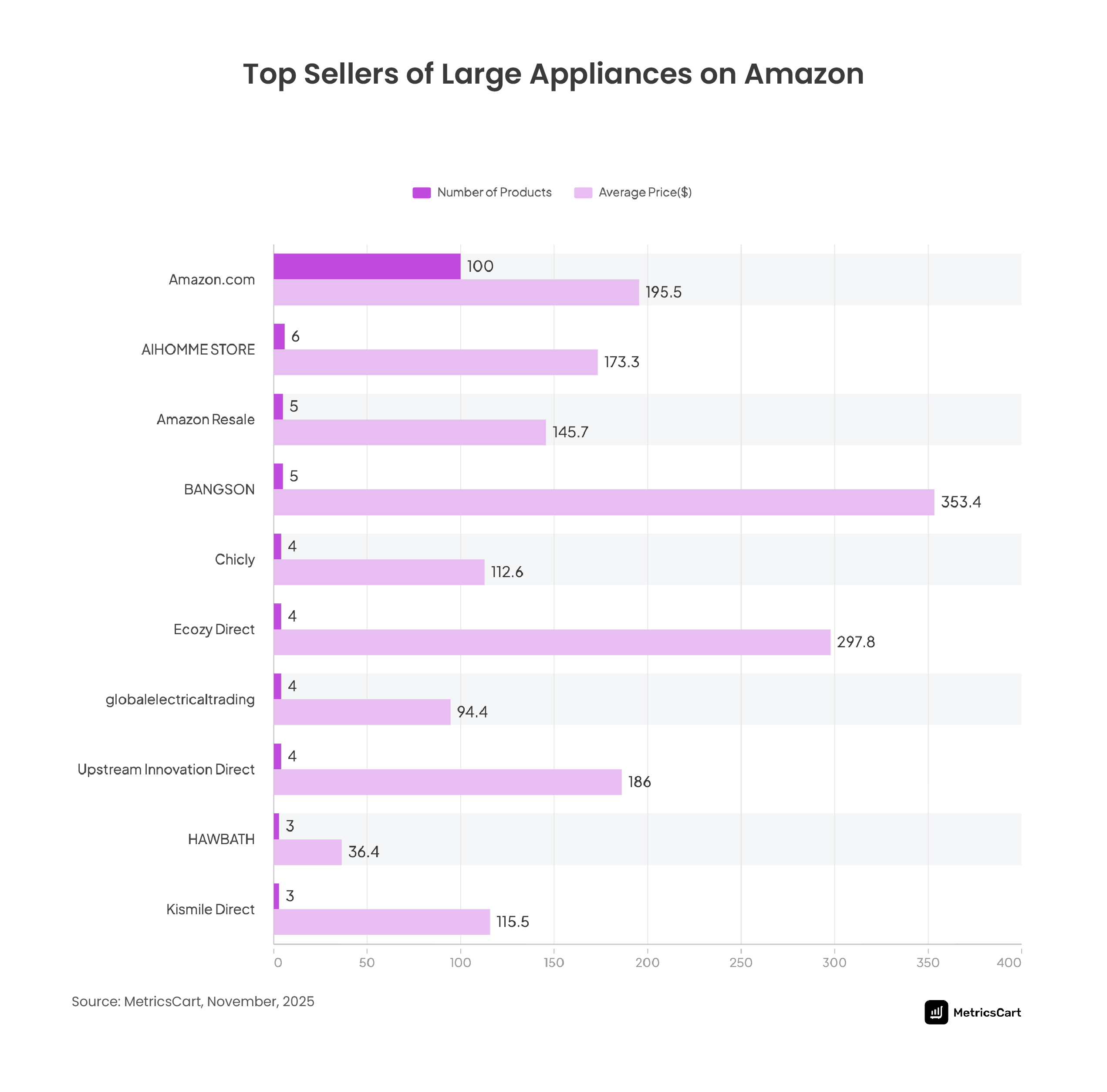

Seller Power Dynamics Driving Large Appliances Bestsellers on Amazon

MetricsCart analysis on Amazon large appliances reveals that marketplace performance is not driven solely by brands, but by which sellers control pricing, inventory, and listing optimization within the Amazon appliances bestsellers list.

Products sold directly by Amazon, the top seller of large appliances, average around $196, placing them slightly above the category’s central price cluster. This positioning suggests a balanced strategy focused on credibility, fulfillment speed, and consistent conversion rates.

Third-party sellers operate across distinct tiers. Premium-focused sellers such as BANGSON average roughly $353 and target higher-margin segments. Meanwhile, budget sellers like HAWBATH average about $36 and compete primarily on affordability and volume among Amazon’s best-selling large appliances.

Seller distribution shows a clear stratification pattern: a small number of sellers dominate higher-priced listings, while a broader group competes in lower price bands. This structure indicates that seller strategy, not just product quality, strongly influences ranking stability.

In Amazon’s ecosystem, distribution control is competitive leverage. Sellers don’t just list products. They shape market positioning.

Large Appliances Best Sellers on Amazon: Actionable Insights for Brands and E-Commerce Teams

Analysis of large appliance bestsellers on Amazon reveals that ranking success is driven by a combination of pricing precision, category selection, and listing consistency, rather than by brand size alone. The following data-backed strategies can help brands and marketplace teams improve visibility and conversion performance.

- Prioritize High-Velocity Categories: Categories like ice makers dominate the Amazon appliances best-sellers list, indicating stronger demand and faster ranking opportunities. Entering high-volume segments increases discoverability and accelerates review accumulation.

- Price Within the Conversion Window: Most Amazon best-selling large appliances in 2025 cluster between $50 and $100. Products priced within this band convert more consistently than extreme budget or premium options. Strategic repricing during competitive periods can significantly improve ranking stability.

- Build Review Momentum Early: Products with high review counts maintain positions even when prices fluctuate. Early review generation campaigns help listings gain ranking resilience and long-term visibility.

- Maintain Listing Consistency: Brands that sustain daily presence in bestseller rankings outperform those with sporadic visibility. Consistent inventory, stable pricing, and optimized listings signal reliability to the algorithm.

- Balance Portfolio Depth and Focus: Only a few brands hold more than ten bestseller listings, showing that catalog breadth increases shelf share. However, concentrated SKU optimization often delivers stronger ranking performance than large but under-optimized catalogs.

- Segment Strategy by Price Tier: Premium brands should compete on differentiation and perceived value, while budget competitors should focus on affordability and conversion velocity. Mixing both strategies within a single catalog can expand digital shelf coverage.

Closing the Charts

Competition in Amazon’s appliance category is expected to intensify as more sellers adopt data-driven optimization strategies. In this environment, the brands that consistently analyze digital shelf signals, adapt quickly, and align with marketplace dynamics will be the ones that sustain visibility and growth.

As the analysis reveals, on Amazon, high-velocity categories dominate rankings, mid-range price positioning drives stronger conversions, and sustained review momentum stabilizes performance. And that means Amazon’s algorithm rewards measurable performance signals more than brand reputation alone.

For brands and e-commerce teams, this underscores the importance of continuous monitoring over periodic analysis. Real-time insights from platforms like MetricsCart enable teams to track ranking movement, pricing changes, and competitor activity as they happen, allowing faster decisions and more precise strategy execution.

Unlock Real-Time Insights With MetricsCart to Win in Amazon’s Large Appliances Category.