About the Report

This Digital Shelf Insights report reviews key performance patterns in the men’s footwear category on Amazon US, with a focus on pricing, assortment depth, review activity, sponsored presence, and seller mix.

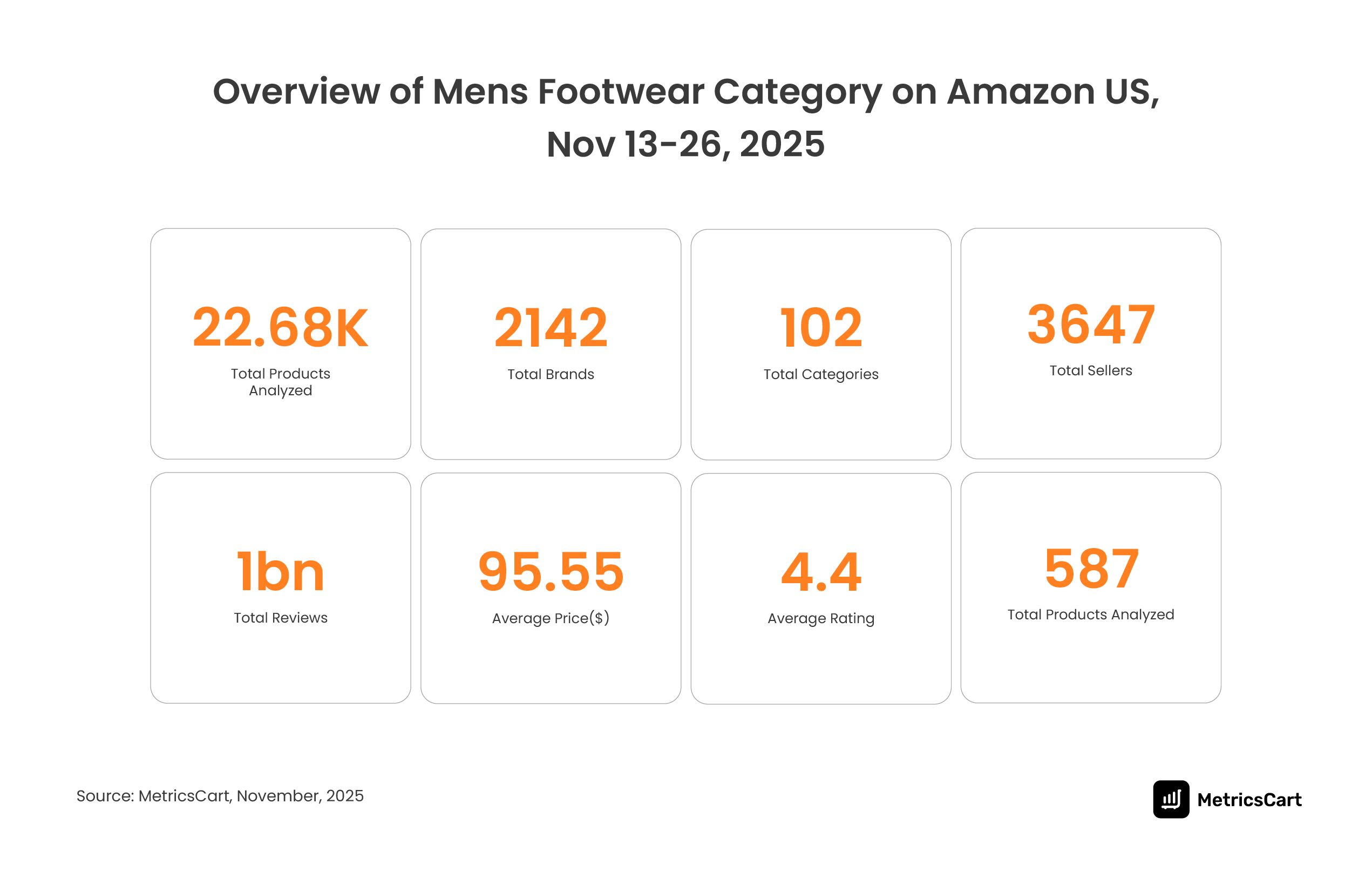

The study tracks the latest men’s footwear trends using the MetricsCart app. It analyzes 22,680 listings observed between November 13 and November 26, 2025.

Introduction

Men’s footwear trends are changing in clear, practical ways. Buying decisions are now driven less by fashion and more by daily use. In the US, the average number of pairs owned by one person is 6.

Changes in how people work and move have shaped this shift. Hybrid jobs and relaxed dress codes have blurred the line between workwear and casual wear.

Leading brands show how this shift is playing out. PUMA has built relevance by focusing on movement and everyday comfort. Campaigns like “Forever Faster” and “Go Wild” highlight footwear designed for everyday wear. This approach aligns with younger shoppers who prefer comfort and self-expression.

Nike reflects the same shift in a different way. The brand stays connected with shoppers beyond the purchase. Tools like interactive product discovery, fitness apps, and digital spaces such as Nikeland keep Nike part of everyday routines.

Shopping behavior has also shifted online. On Amazon US, this has shortened decision cycles, with men favoring footwear that shows strong ratings, high review volume, and clear comfort benefits at the point of search.

Let us understand how these shifts are reflected in what men buy, how brands compete, and which product attributes drive visibility and sales across the category.

Highlights

- Amazon US men’s footwear includes 22.68K products, 2,142 brands, and 3,647 sellers, generating nearly 1 billion reviews with an average rating of 4.4.

- Fashion Sneakers lead with 3,998 products, while Hiking Boots ($135.7) and Industrial Boots ($132) hold the highest average prices.

- Nike leads the men’s footwear category on Amazon US, followed by Skechers and adidas as the next most prominent brands.

- Prices range from $5.9 to $2,549, showing that brands perform best in clear premium or budget positions.

- Crocs Classic Clog leads with 138M reviews at ~$35, while $9–$10 flip-flops generate 20–39M reviews, and most brands sponsor fewer than 20 products.

Overview of Men’s Footwear Category on Amazon US

This analysis draws on data extracted through the MetricsCart app to examine the men’s footwear category on Amazon US between Nov 13 and Nov 26, 2025. The dataset covers 22.68K products listed across the platform.

The men’s footwear category includes 2,142 brands across 102 categories and is supported by 3,647 active sellers. This highlights the scale and fragmentation of competition within men’s footwear on Amazon US.

Overall, shopper engagement is high, with nearly 1 billion total reviews recorded across products. The category shows an average product price of $95.55 and an average rating of 4.4, indicating strong demand and generally positive customer sentiment.

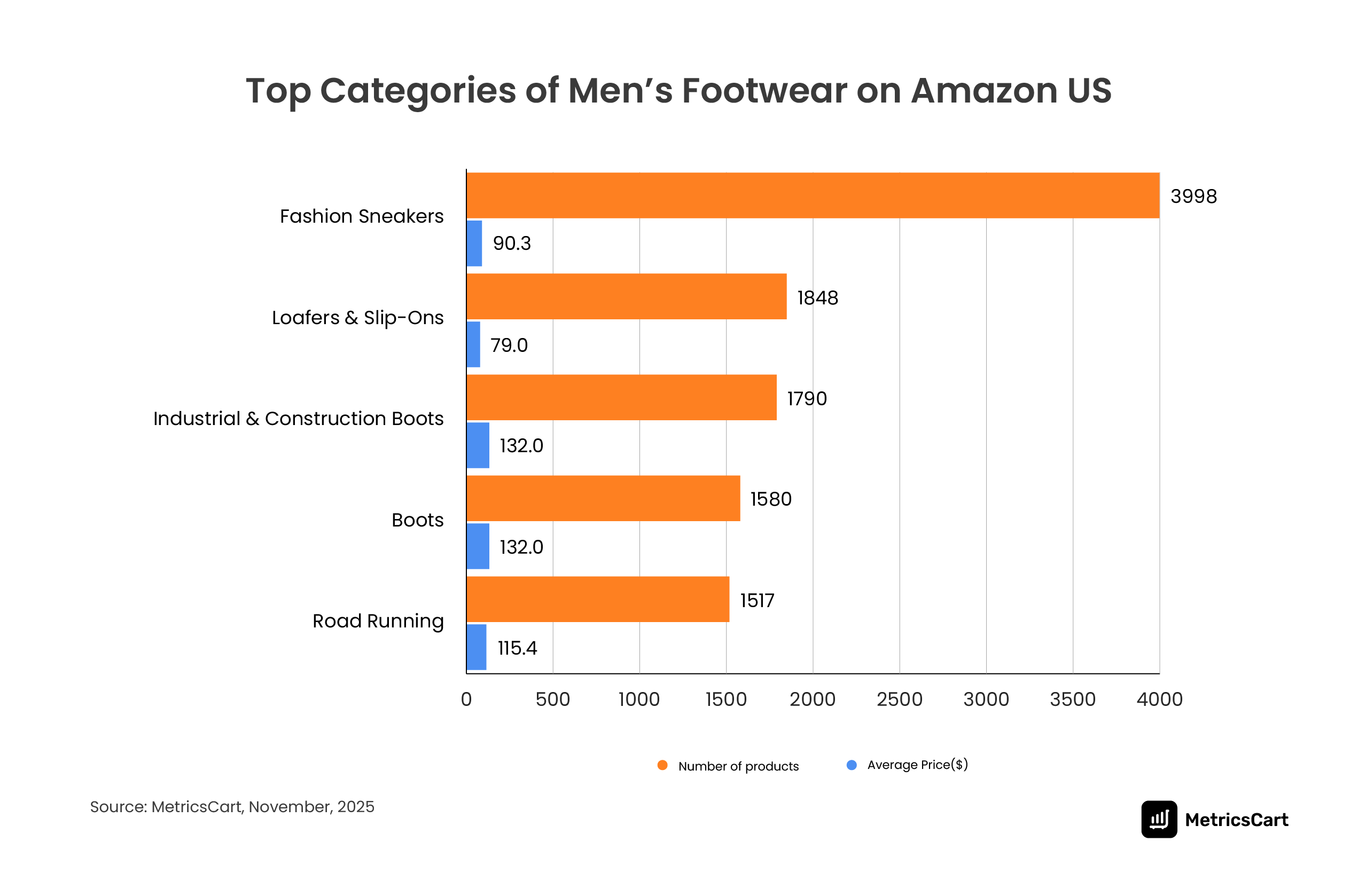

Fashion Sneakers Lead Volume, While Utility Footwear Drives Higher Prices

The men’s footwear category trends on Amazon US are extensive. The top categories by product count include Fashion Sneakers (3,998), Loafers & Slip-Ons (1,848), and Industrial & Construction Boots (1,790), followed by Boots (1,580) and Road Running (1,517).

Fashion Sneakers lead with 3,998 products and an average price of $90.3, which makes them the largest and one of the most competitive segments.

This happens for a few reasons that are evident in marketplace behavior.

- First, sneakers support endless variations (colors, materials, collaborations), which increases SKU count.

- Second, sneakers are highly search-driven; shoppers browse and compare heavily in this segment.

- Third, the rise of athleisure and fashion-forward collaborations (e.g., between lifestyle and sports brands) keeps this category dynamic.

- Finally, many private labels and emerging DTC brands compete here, increasing product volume.

Utility categories behave differently. They are designed for specific use cases, not for everyday wear.

Hiking Boots (avg $135.7) and Industrial & Construction Boots (avg $132) are priced higher, even though their product counts are smaller than those of sneakers. They often use specialized materials such as steel toes, waterproof membranes, reinforced soles, and insulation.

These functional requirements increase production costs and support higher average prices, while narrower use cases naturally yield fewer product listings than mass-market sneakers.

Road-running shoes are priced around $100, between sneakers and boots. Buyers in this segment look for comfort, support, and injury prevention. They are willing to pay more than casual sneaker buyers, but still compare options closely.

Together, the data show a clear split: sneakers drive volume through everyday relevance, while utility and performance footwear hold pricing power through purpose-led demand.

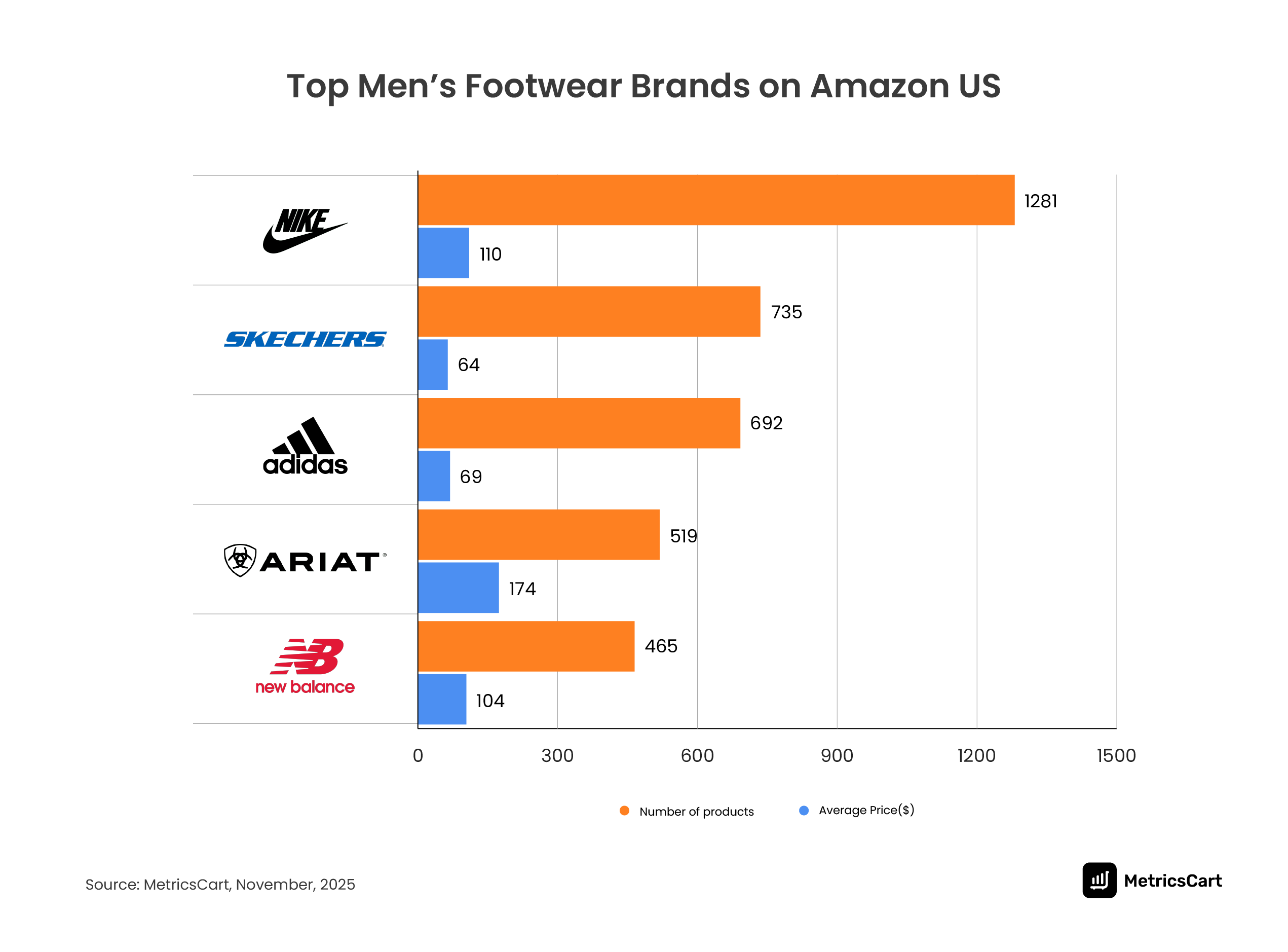

Top Men’s Footwear Brands on Amazon US: Nike Leads, Followed by Skechers and adidas

Using the MetricsCart app, we found that men’s footwear brands with larger assortments hold a clear visibility advantage on Amazon US. Nike leads the category with 1,281 active listings, followed by Skechers (735) and adidas (692).

Nike’s scale translates directly into shelf presence. A wider catalog allows the brand to surface across multiple consumer intents, including lifestyle, running, and training. This consistent visibility supports Nike’s higher average price of $110, where brand trust and performance positioning reduce price sensitivity.

Skechers and adidas compete at lower price points, averaging $64 and $69, respectively. Their performance is driven by familiarity and value positioning. For price-conscious shoppers, these brands offer a balance of comfort, recognition, and affordability, which lowers purchase hesitation.

Premium brands such as Ariat ($174) and ROCKY ($149) operate at the upper end of the price spectrum. Their assortments focus on work and utility footwear, where durability and protection are primary purchase drivers. In these segments, functional reliability outweighs fashion considerations.

PUMA, with an average price near $65, remains positioned for volume. Its pricing supports repeat purchases and broad reach, allowing the brand to compete effectively within the mid-price range without relying on premium positioning.

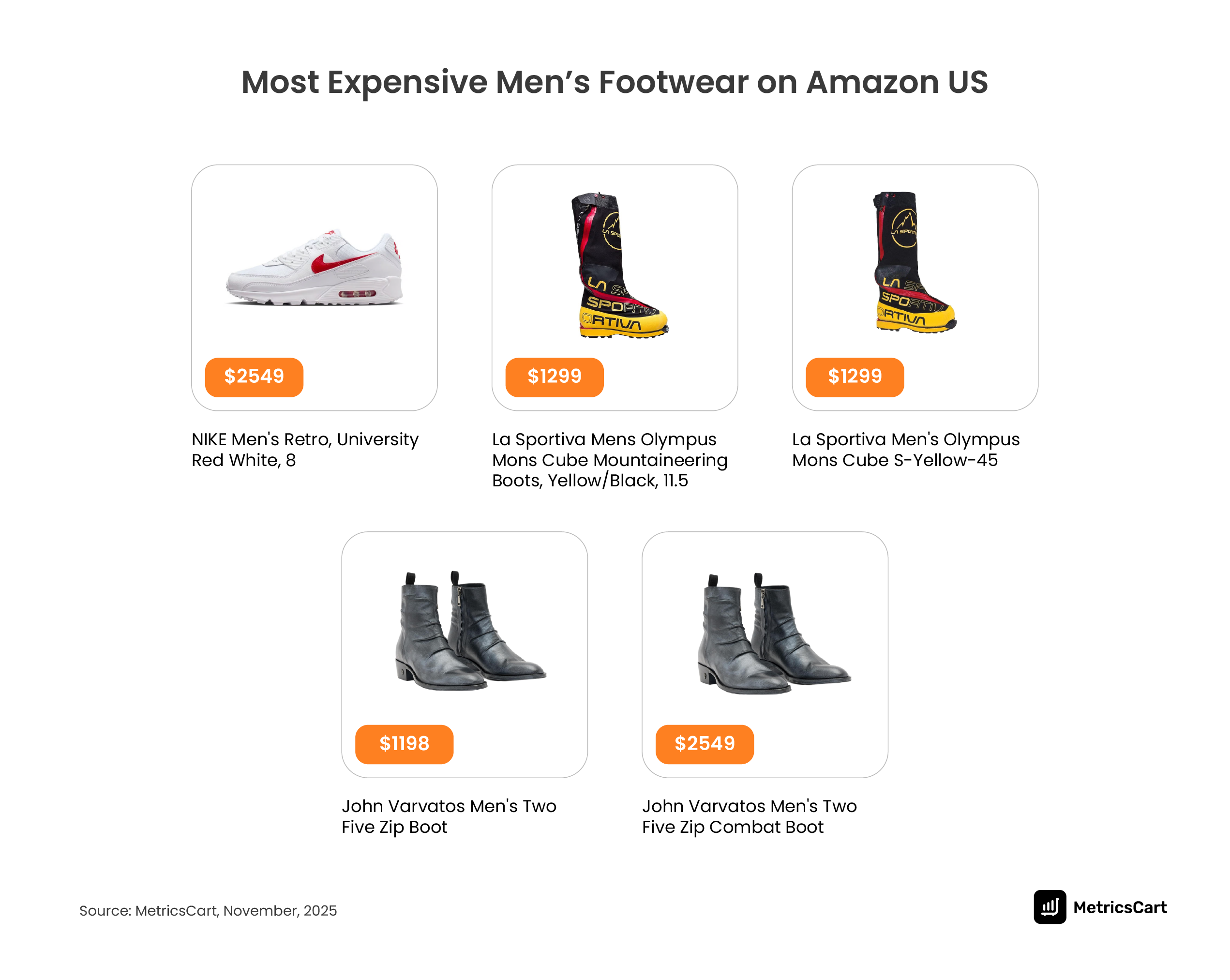

SEEKWAY Water Shoes Are the Most Affordable, While NIKE Men’s Retro Is the Most Expensive

The MetricsCart app shows that premium pricing in men’s footwear on Amazon US is limited to a very small set of products. Only a few listings exceed $1,000, indicating that high pricing is not widespread across the category.

The highest-priced product in the period is NIKE Men’s Retro, University Red White, listed at $2,549. This price sits far above the rest of the market and functions as an outlier rather than a benchmark.

This position is driven primarily by brand strength and limited availability. Buyers searching for this product show high intent and low price sensitivity. As a result, pricing is less constrained than that of similar products.

The next-highest-priced item is the La Sportiva Olympus Mons Cube mountaineering boots, priced at $1,299. These products serve extreme-use scenarios where performance and safety are critical. Pricing reflects technical design and low tolerance for failure.

In this segment, high prices persist because options are limited and the risk of substitution is low. Demand is small but focused, allowing premium prices to hold without relying on volume.

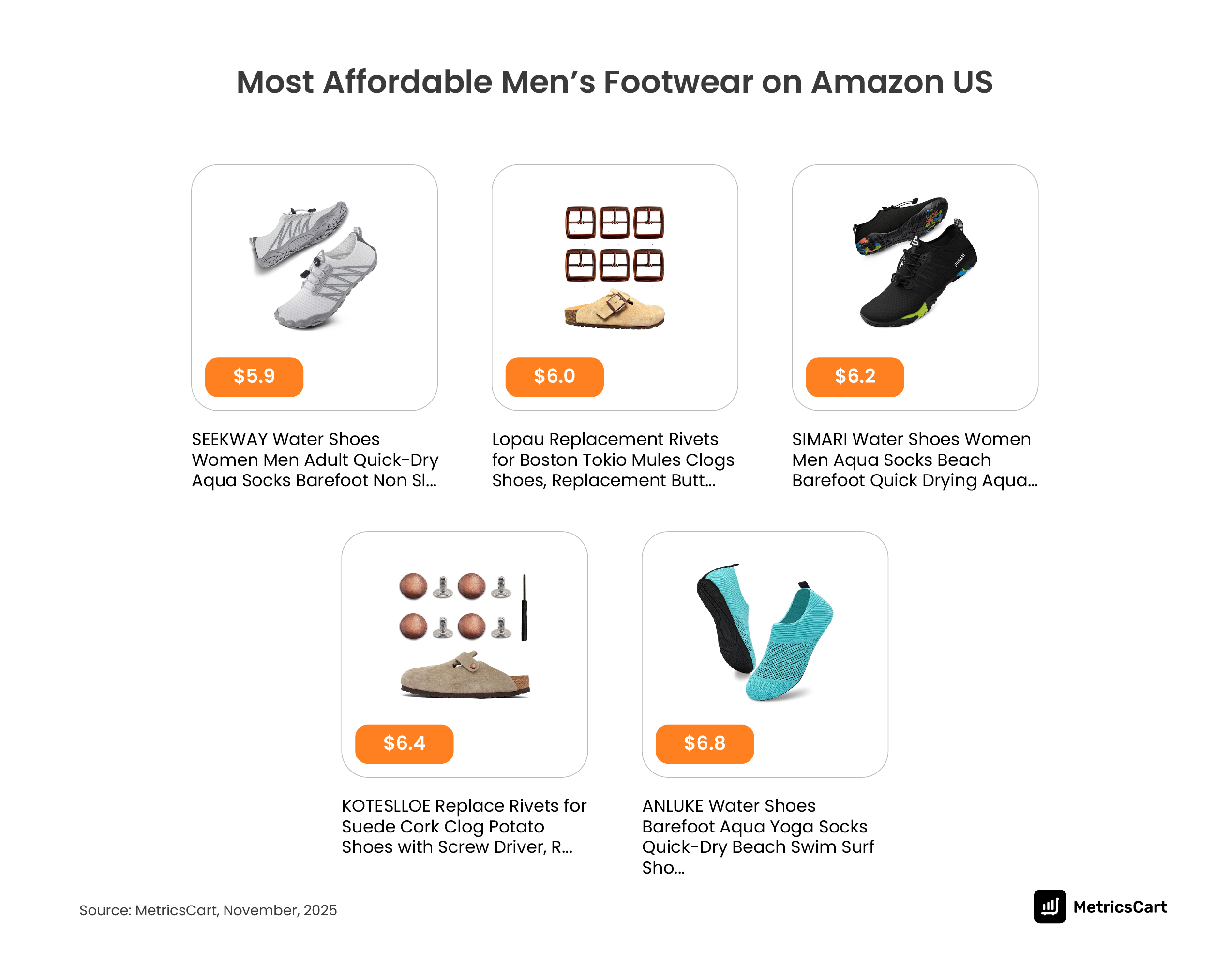

At the lower end of the price range, pricing behaviour changes sharply.

The lowest-priced products include SEEKWAY Water Shoes ($5.9), SIMARI Water Shoes ($6.2), and clog replacement rivets. These items are functional products designed for short-term or specific use.

Their low prices are driven by simple construction, basic materials, and limited feature variation. These factors reduce production costs and allow many sellers to compete at similar price points.

High substitutability keeps prices anchored near the category floor. Any upward price movement increases the risk of losing visibility and conversion to similar alternatives.

In this segment, performance depends less on brand positioning and more on search presence, delivery speed, and clear pricing. Purchases are task-driven, with short decision cycles and limited repeat loyalty.

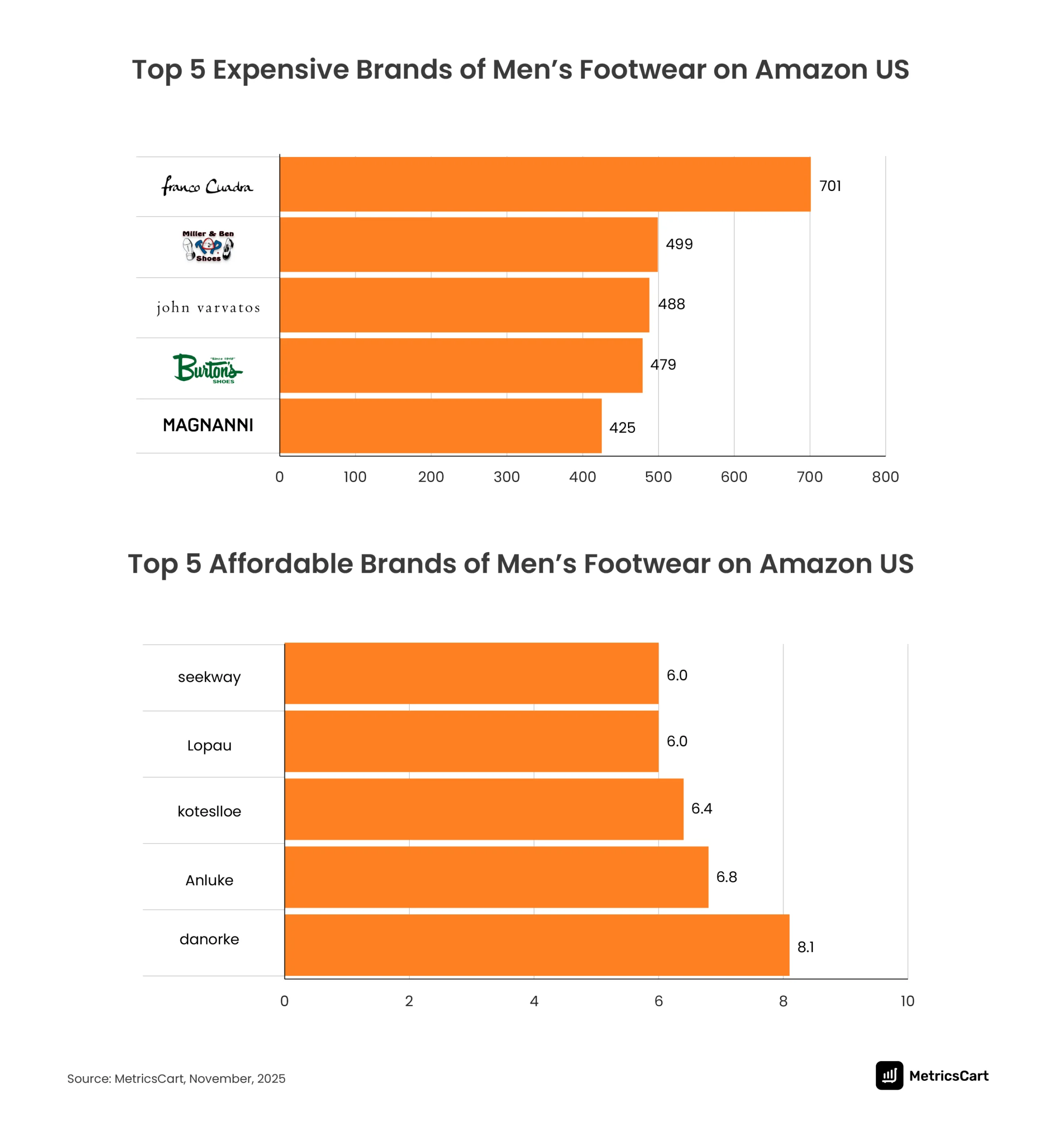

Franco Cuadra Emerges as the Most Expensive Brand, While Danorke Wins the Budget Segment

Top 5 Affordable Brands of Men’s Footwear on Amazon US

Premium brands, such as Franco Cuadra ($701), Miller & Ben ($499), John Varvatos ($488), and Magnanni ($425), top the price range for men’s footwear on Amazon US. These brands focus on leather boots and dress shoes, which are typically purchased for work, formal occasions, or long-term wear.

Shoppers in this segment use price as a signal of quality and reliability. When footwear is expected to last longer or be worn frequently, buyers focus on materials, comfort, and build. Price becomes a secondary factor. This allows premium brands to maintain higher average prices. Their role in the market is to serve lower-frequency, higher-value purchases.

Affordable brands such as Danorke ($8.1), Anluke ($6.8), Koteslloe ($6.4), Seekway ($6.0), and Lopau ($6.0) operate at the opposite end of the market. These products are commonly used for water activities, indoor wear, or short-term needs. Buyers do not expect long-term durability at this price level.

In this segment, decisions are driven by convenience and cost. Shoppers aim to solve an immediate need with minimal risk. As a result, these brands compete on price and availability.

Together, the data shows a clear split in men’s footwear demand on Amazon US. Premium brands succeed by delivering durability and use-specific value. Budget brands grow by meeting quick, low-commitment purchase needs.

While pricing plays an important role in shaping consumer purchase behavior, reviews often tip the balance toward conversions.

Let’s analyze the MetricsCart research team’s findings to see how review volume, particularly for everyday comfort products, adds an extra layer of consumer trust.

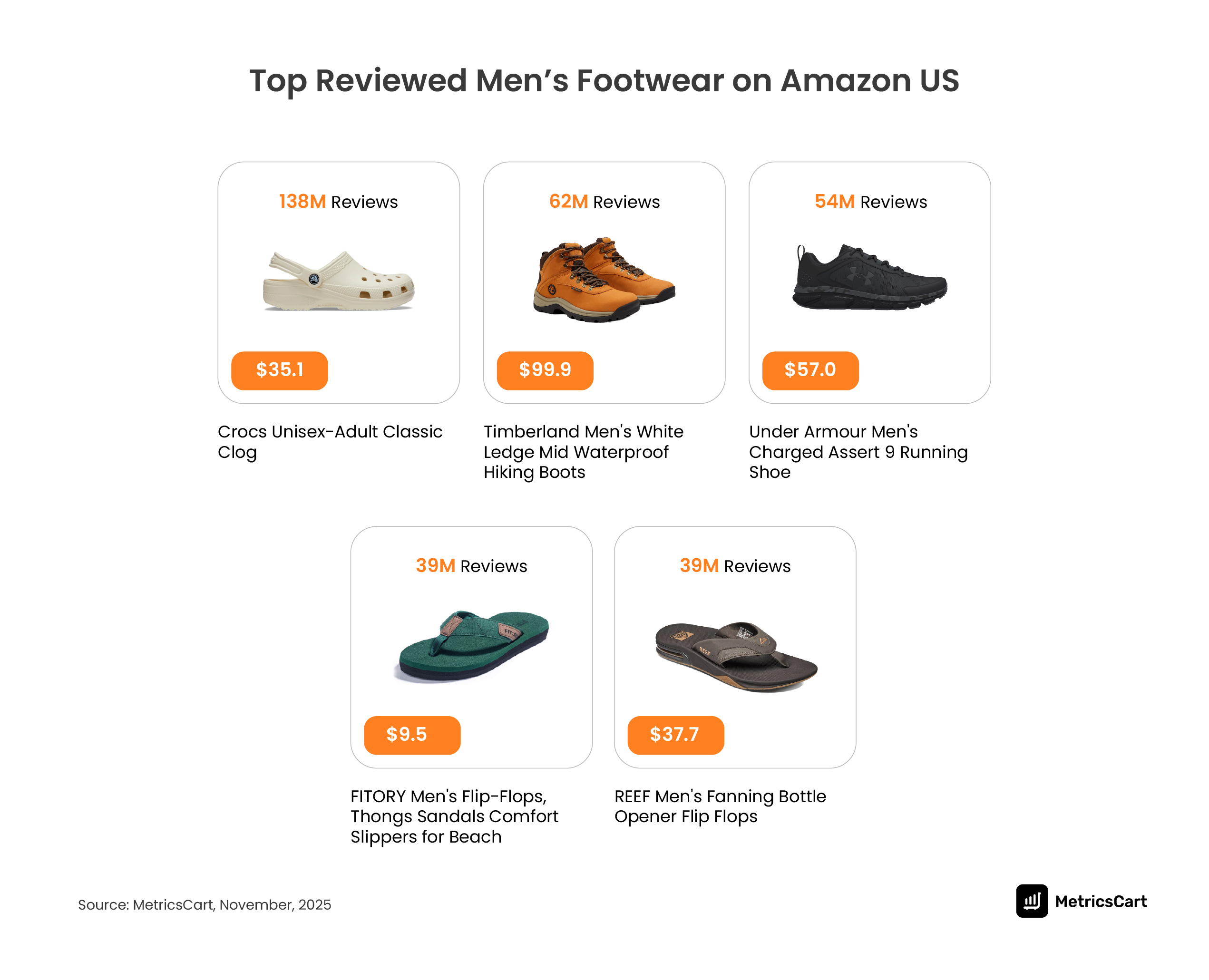

Crocs, Timberland, and Under Armour Lead Review Volume in Men’s Footwear

The strongest demand signal in this dataset is review volume, which highlights the best Amazon shoes for men based on repeat use. The review curve is evidently dominated by everyday comfort products.

Crocs Classic Clog leads with 138M reviews at a low average price of about $35.Crocs is not winning because it is new. It wins because it is repeatedly worn and purchased, creating a steady stream of reviews. That review momentum becomes the foundation for building trust with new shoppers. Here, purchases increase, resulting in a high volume of reviews.

The rest of the top-reviewed list supports the same story:

- Timberland has 62M reviews at about $99.9.

- Under Armour has 54M reviews at about $57.0.

- Multiple flip-flops have 39M reviews at $9.5–$37.7, showing that both “daily comfort” and “low price impulse” can drive huge review volumes.

One key factor driving this trend is price sensitivity. Flip-flops priced at $9–$10, such as FITORY and KuaiLu, generate 20M–39M reviews, which is notably high for such low-cost items. This happens because low-priced products reduce buyer hesitation, encouraging trial and quick purchases.

As a result, these products capture more volume, leading to higher review counts. In the case of footwear, where fit can be a barrier, a $9 purchase feels lower-risk than a $90 one.

READ MORE | Crocs didn’t win Amazon US by accident. See how the $4B shoe brand dominates reviews and demand. Crocs Marketing Strategy: Insights Into The $4 Billion “Ugly Shoe” Brand

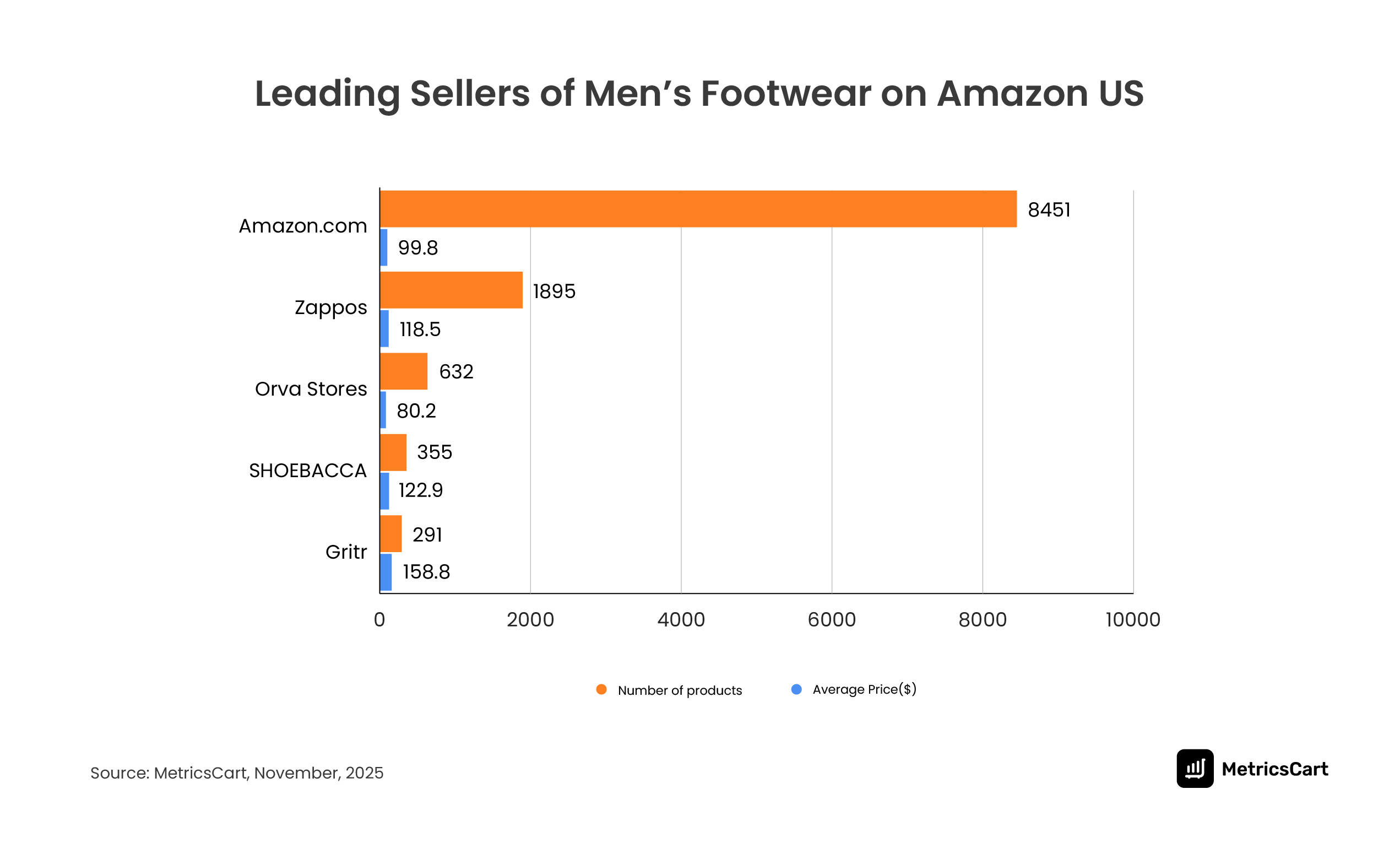

Seller Landscape: Amazon.com Dominates Men’s Footwear, Followed by Zappos

Based on MetricsCart research team’s analysis, seller concentration in men’s footwear on Amazon US is highly skewed toward a small number of large sellers. Amazon.com leads with 8,451 active listings, followed by Zappos with 1,895.

Beyond these two sellers, listing volume declines sharply, with most sellers offering only a few hundred products or fewer.

Amazon.com leads because it controls the full buying experience. Shoppers find more options in one place, see competitive prices, and get fast delivery with easy returns.

This matters in footwear, where fit issues are common, and return risk is high. Amazon’s reliability reduces hesitation and increases conversion, making it the default seller for many buyers.

Beyond Amazon.com and Zappos, the seller base includes players such as Shoe Carnival, Shoes For Crews, Rockport, Clarks, and several brand-direct and third-party sellers.

Many focus on niche products or short-term pricing gaps. However, fewer listings and weaker fulfillment reduce their presence in search results. As a result, their impact stays limited.

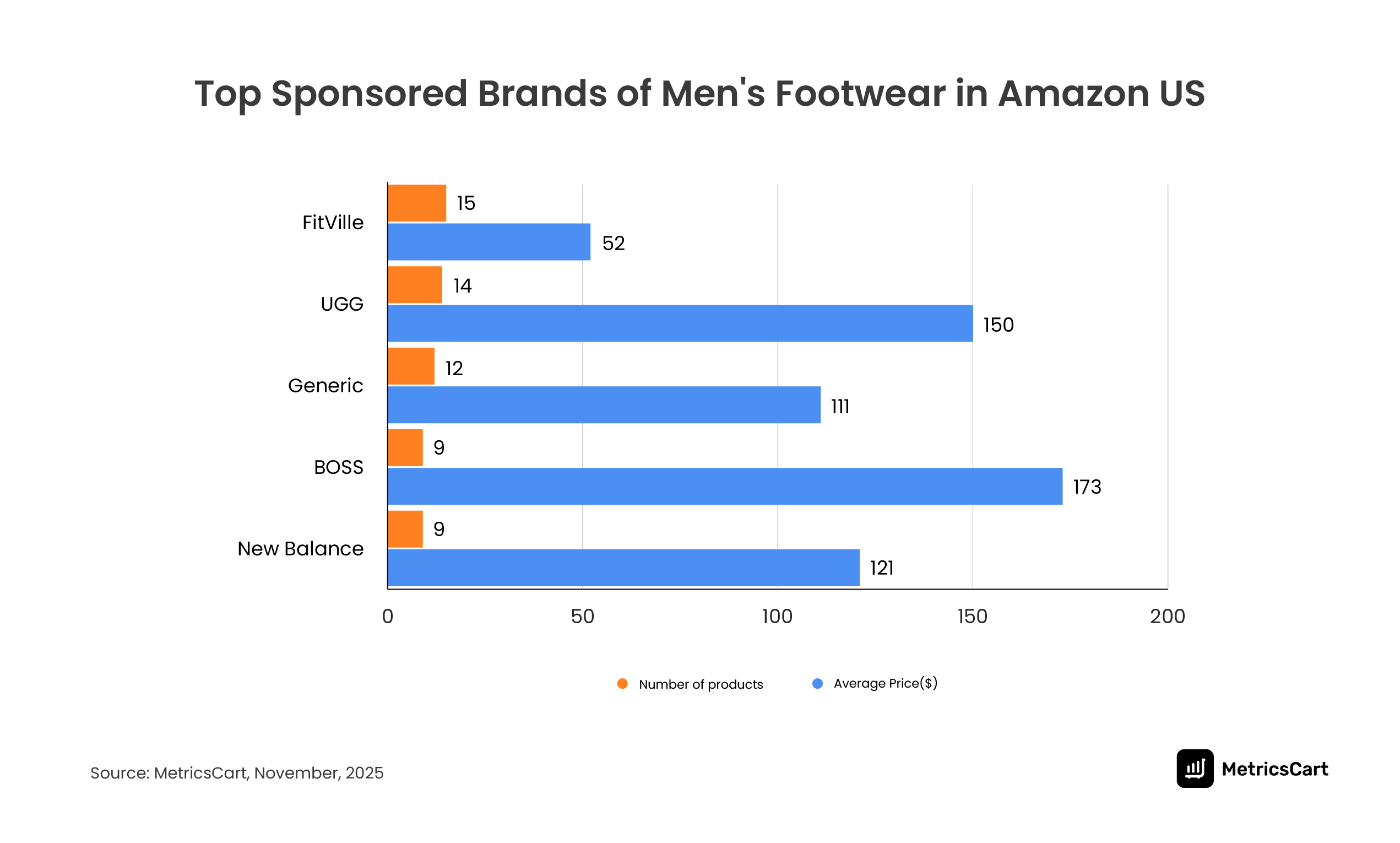

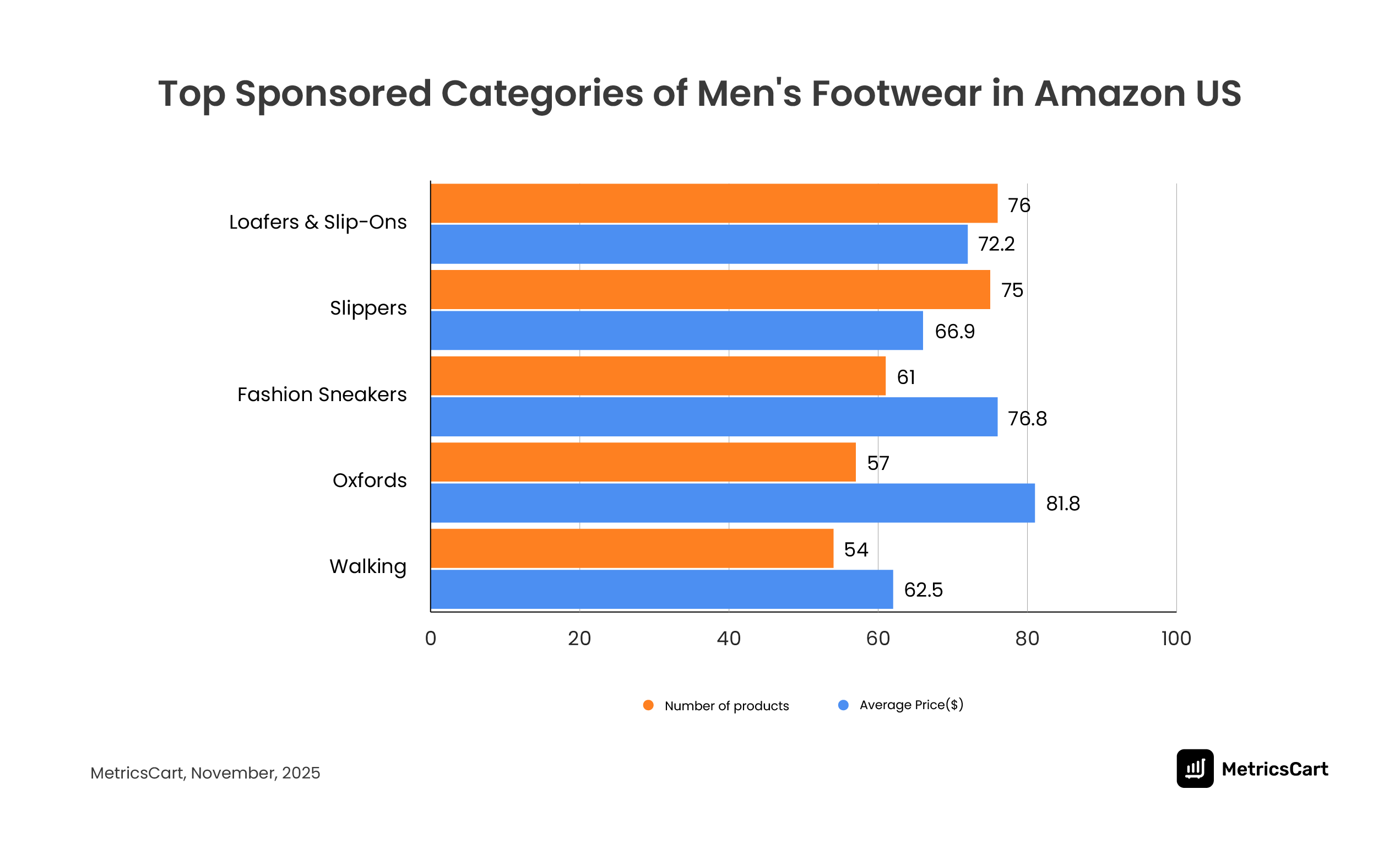

Sponsored Ads in Men’s Footwear: Brand and Category Patterns

Sponsored activity in men’s footwear on Amazon US is focused, not broad. Brands promote a small set of products rather than their full catalog. FitVille and UGG lead sponsored brand activity with 14 promoted products each, followed by Generic (12) and Rockport (11).

This shows that even large brands concentrate spending on a few SKUs that are more likely to convert.

Loafers & Slip-Ons (76 sponsored products) and Slippers (75) receive the highest ad support, followed by Fashion Sneakers (61) and Oxfords (57).

These categories have many similar-looking options and tight price ranges. Ads help brands gain visibility where shoppers can quickly compare and switch.

Functional categories rely less on ads. Industrial & Construction Boots (32) and Hiking Boots show lower sponsored presence despite higher prices. Buyers in these segments search with intent and spend more time reviewing details. Performance and fit matter more than placement, which reduces the need for aggressive ad spend.

Overall, sponsored ads are used to defend share in crowded, everyday categories. They play a smaller role where purchase decisions are slower and driven by function or need.

When viewed together, these patterns explain how visibility, pricing, and purpose interact on the digital shelf.

What the MetrcsCart InsightsIs Saying to Footwear Brands

- Scale comes from repeated use cases, not from broader catalogs. Categories like Fashion Sneakers (3,998 SKUs) and Loafers & Slip-Ons (1,848 SKUs) lead because they meet daily-wear needs. Brands grow by repeating what works, not by adding new categories.

- Pricing power depends on purpose. Hiking Boots ($135.7) and Industrial & Construction Boots ($132) sustain higher prices because buyers enter with clear job or outdoor needs. Price sensitivity is lower when footwear failure carries risk.

- Low prices win only where risk is low. Brands priced under $10 succeed mainly in water shoes, indoor wear, or short-term use. Buyers trade durability for speed and convenience in these cases.

- Crowded categories still reward clarity. High SKU density in sneakers and loafers reflects steady demand rather than saturation. Brands that clearly communicate fit, comfort, and everyday value continue to win shelf space.

Put Your Best Foot Forward

As the men’s footwear market on Amazon US continues to evolve, understanding consumer behavior and market trends is essential.

MetricsCart’s data-driven insights provide brands with the tools to make informed decisions, stay responsive to shifts, and maintain a competitive edge in a rapidly changing landscape.

Disclaimer: MetricsCart is the sole owner of the data used in this Digital Shelf Insights report. Any third-party use requires proper attribution.

Looking to lead the way in the US footwear space?