Highlights

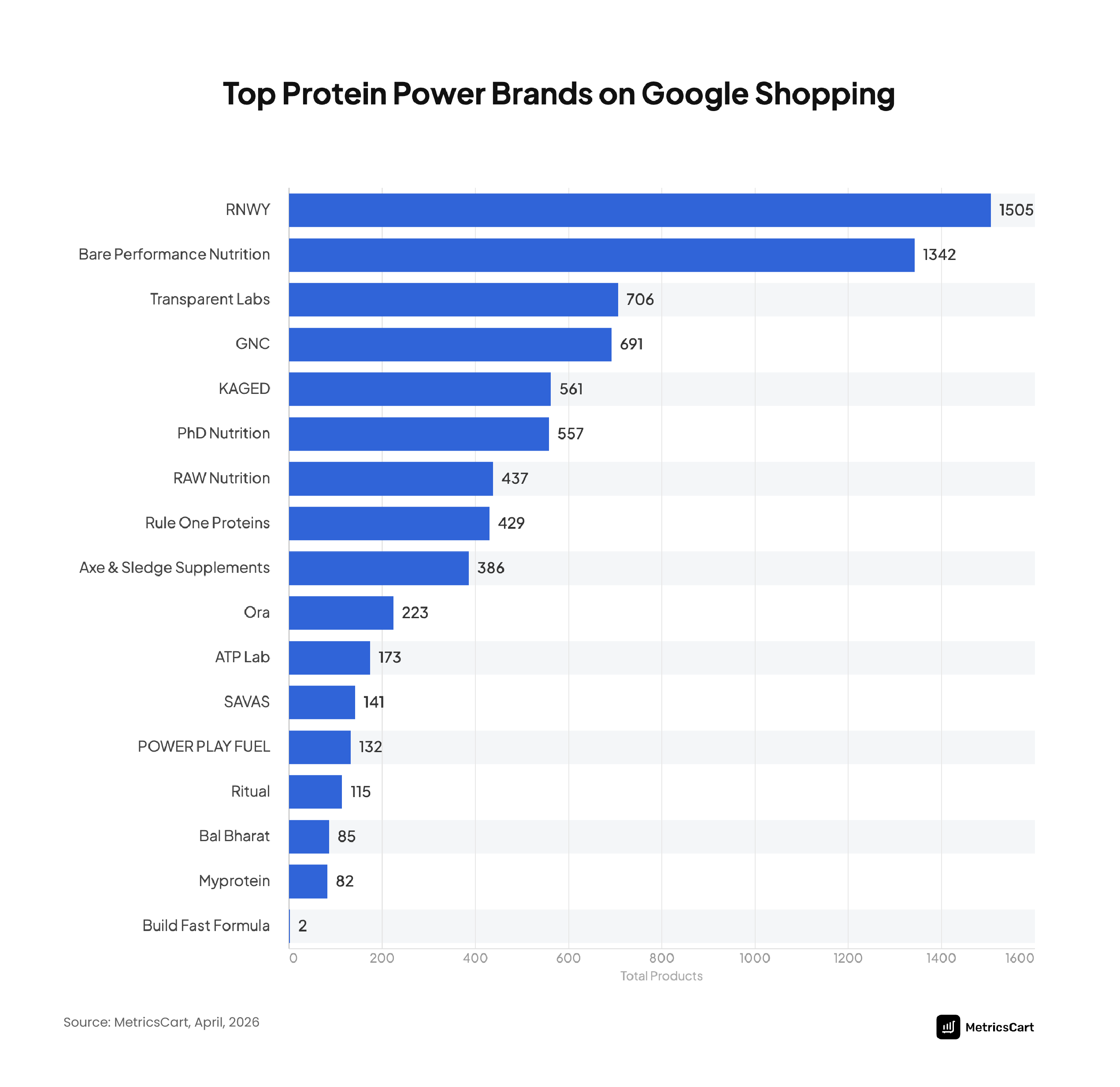

- RNWY and Bare Performance Nutrition are the most visible, with 1,505 and 1,342 listings, respectively. Transparent Labs and GNC hold a strong mid-tier presence (~700 products each), while many niche brands have minimal shelf space.

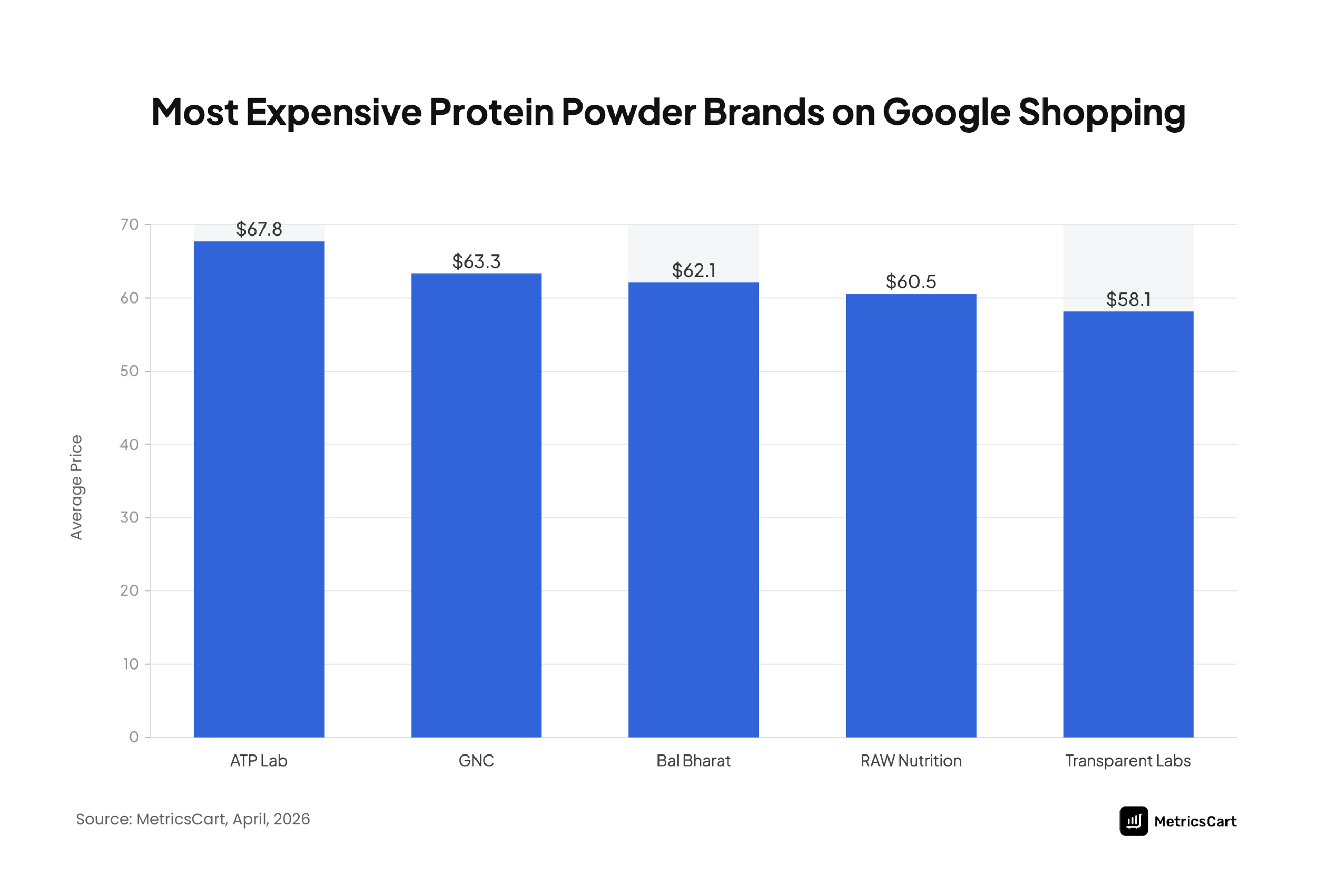

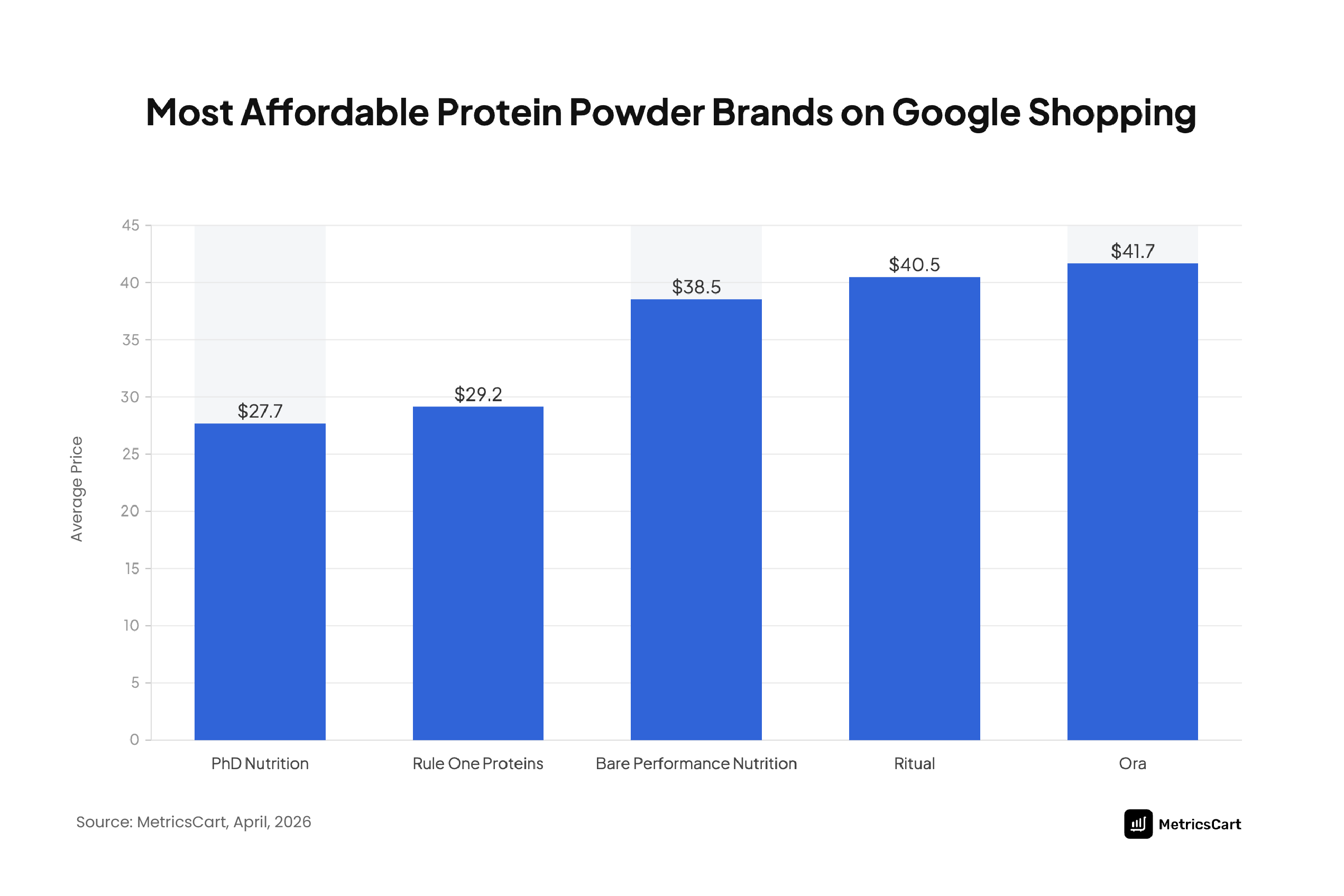

- ATP Lab leads the premium segment (avg. price $67.75), followed by GNC ($63.31) and Bal Bharat ($62.09). In contrast, PhD Nutrition ($27.72 avg.) and Rule One Proteins ($29.16) target budget-conscious shoppers.

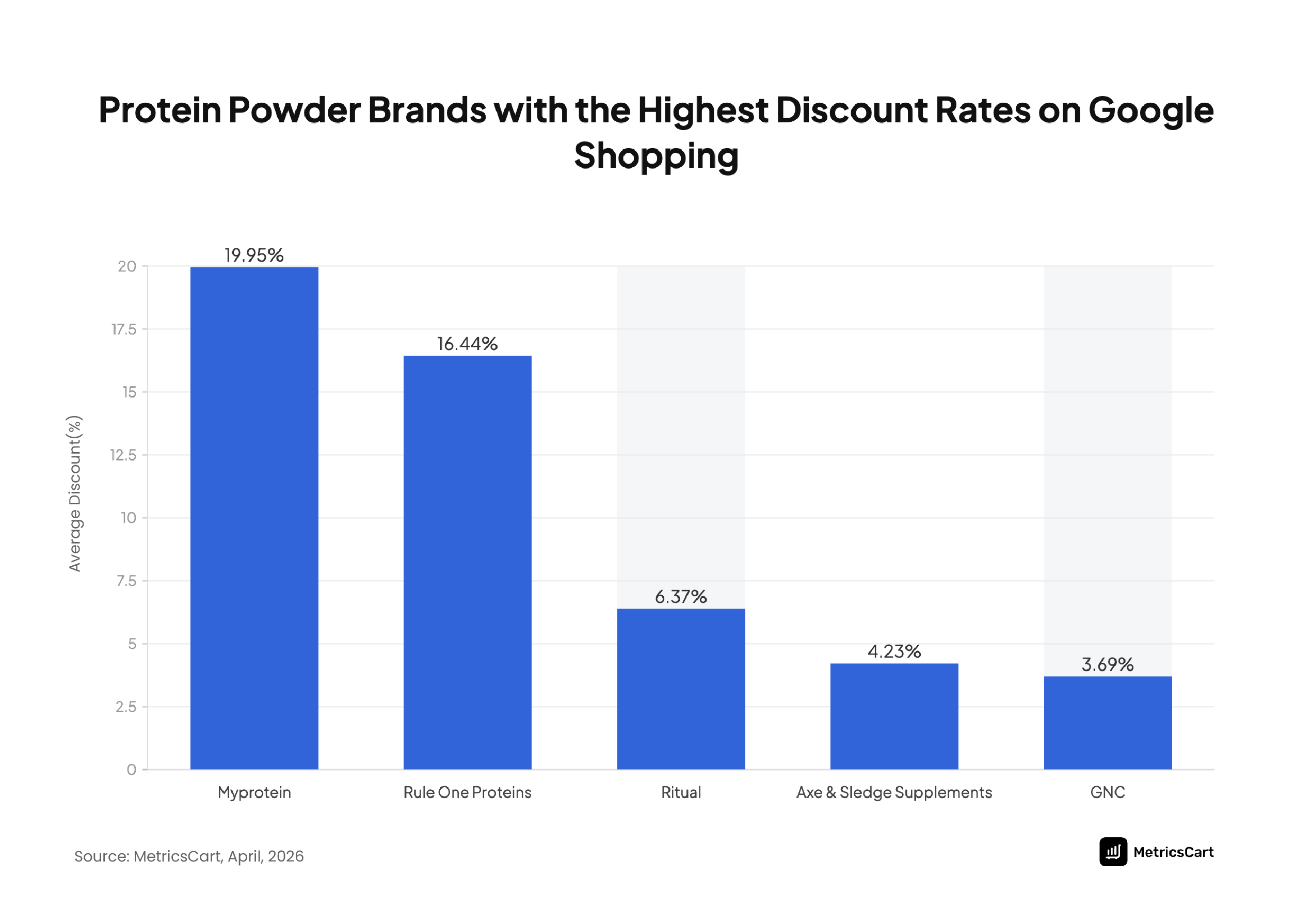

- Myprotein stands out with an average discount of nearly 20%, indicating an aggressive promotional strategy. Rule One Proteins also offers heavy discounts (16.4%). By contrast, GNC and Axe & Sledge offer minimal discounts, relying more on brand strength than price cuts.

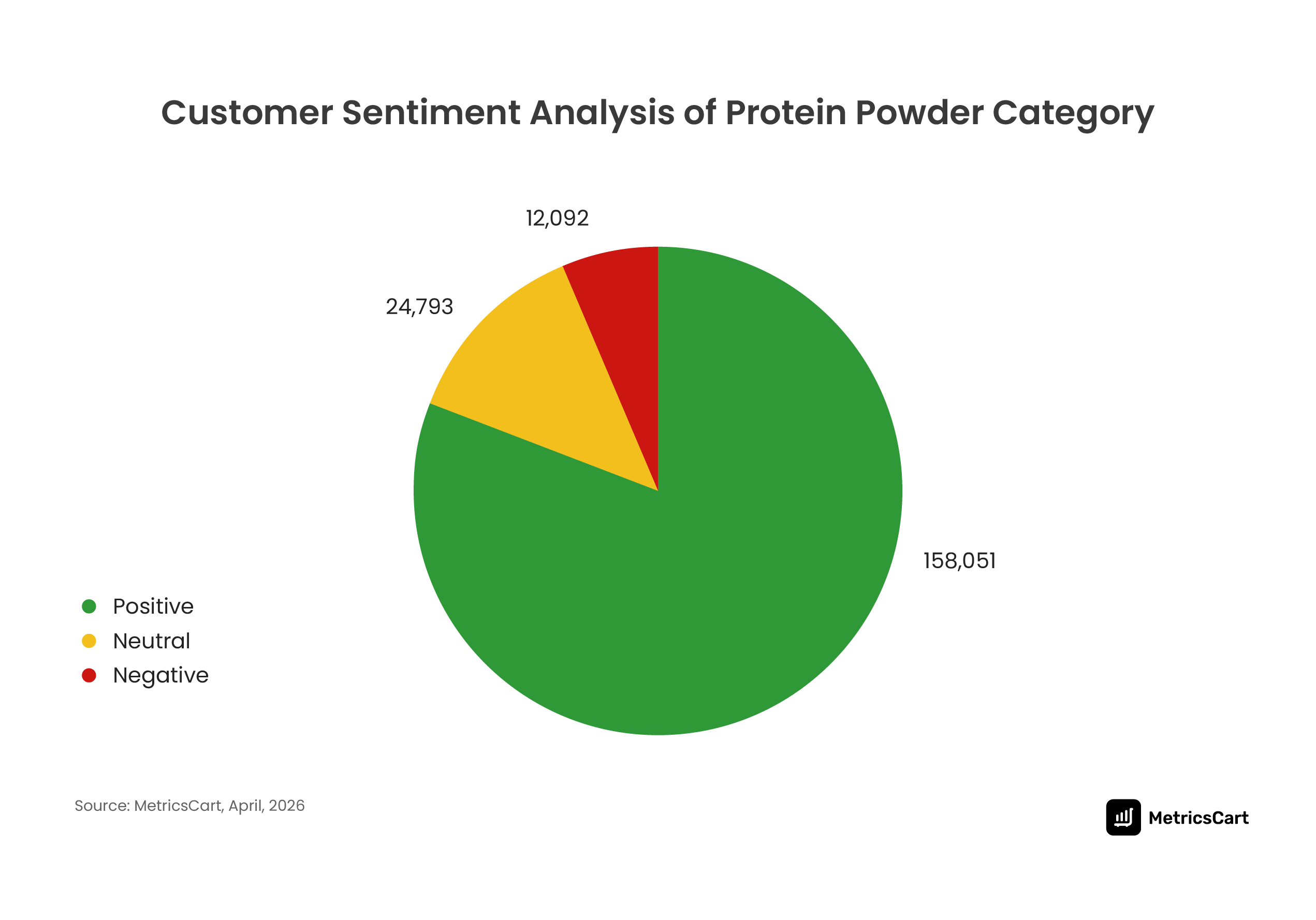

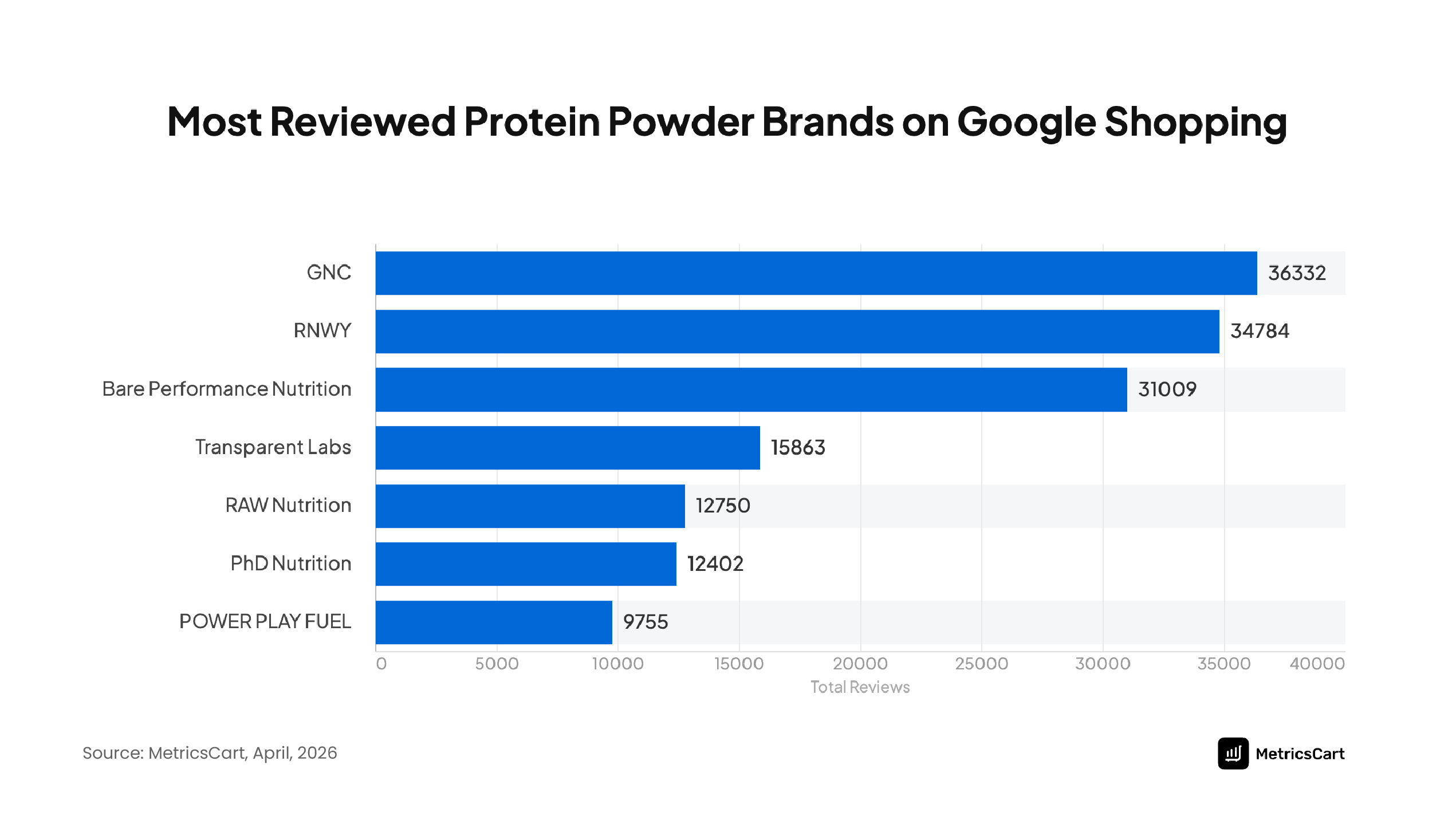

- Consumers are highly satisfied overall, with 158,051 positive reviews vs. just 12,092 negative reviews. GNC leads in review volume (36,332 reviews), followed by RNWY (34,784) and Bare Performance Nutrition (31,009).

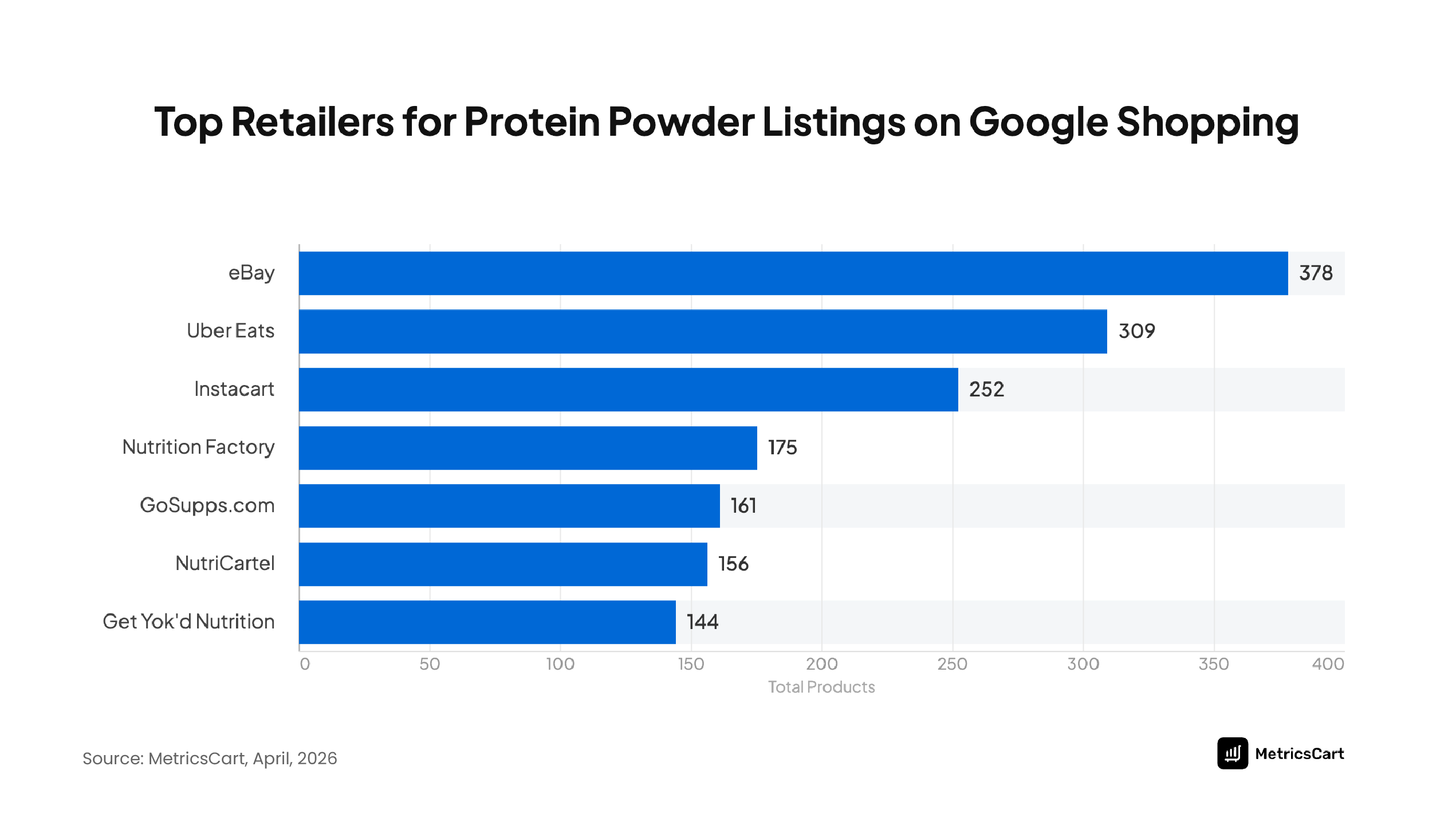

- eBay is the #1 buying option for Google Shopping protein powders (378 listings), with Uber Eats (309) and Instacart (252) also in the top three. This highlights a new quick-commerce trend in supplements.

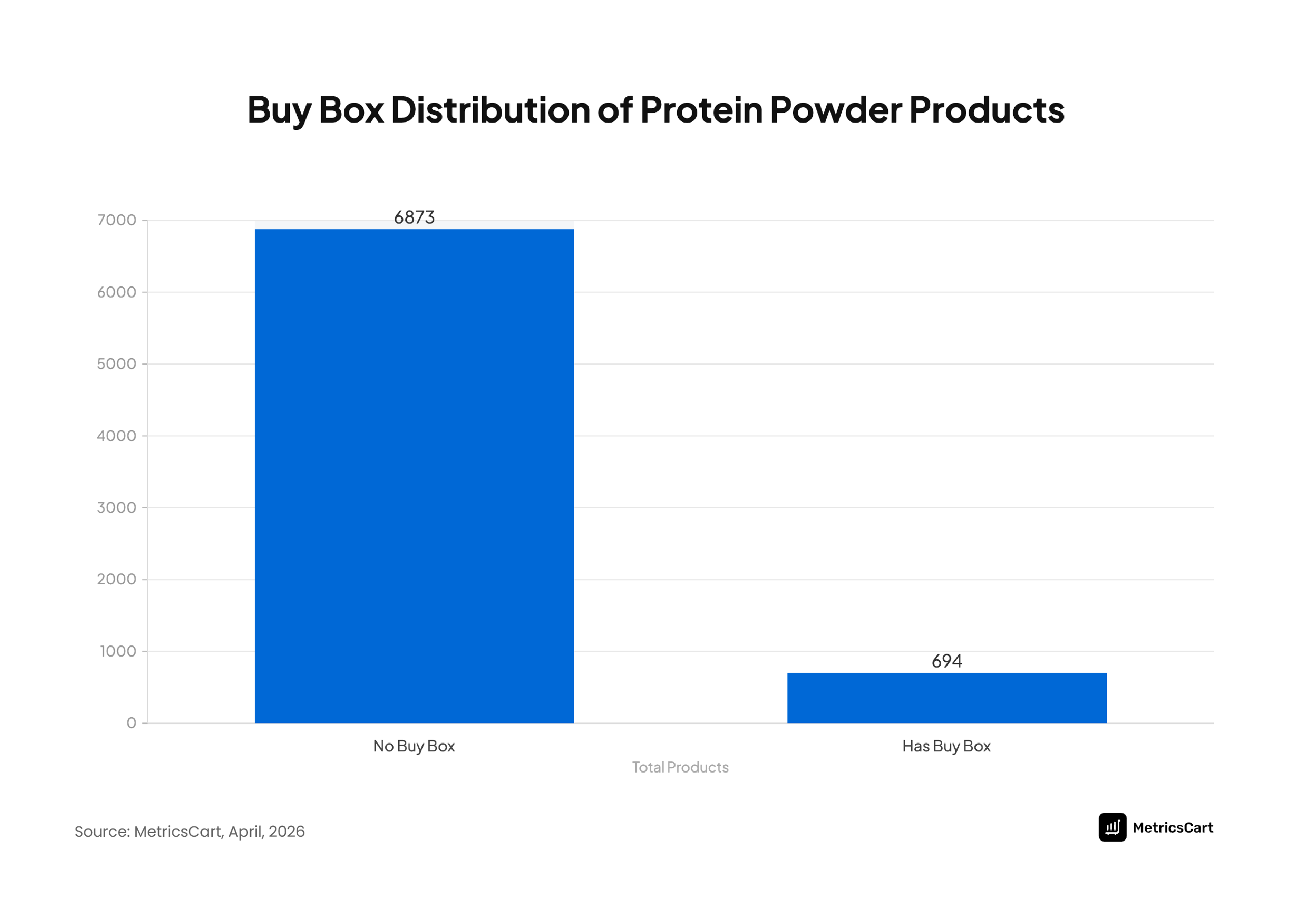

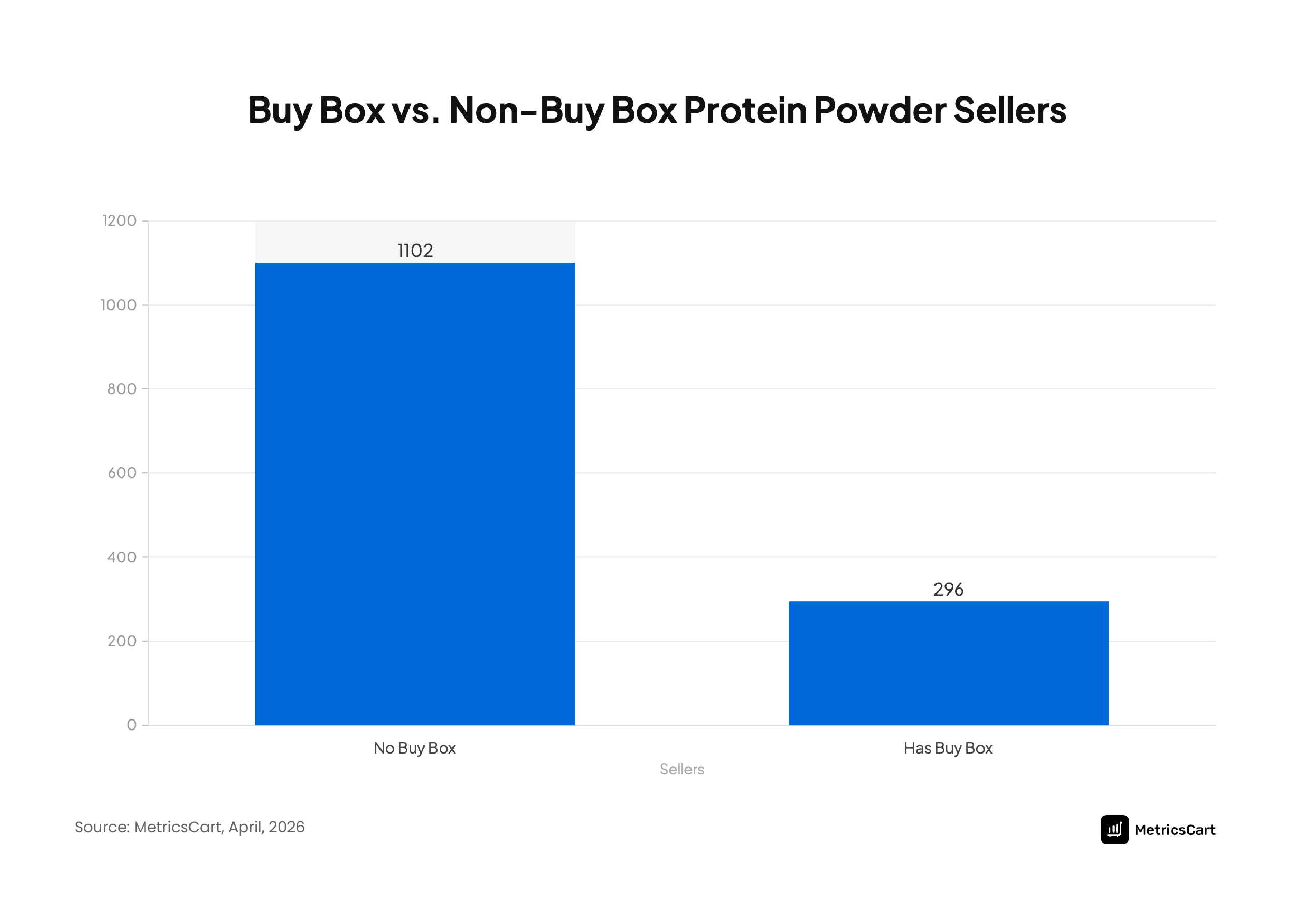

- Only 694 products (≈9%) have the Buy Box, while 6,873 products (91%) do not. In other words, 91% of listings are buried without the featured Buy Box. Likewise, just 296 sellers (21%) ever win the Buy Box, versus 1,102 sellers who never do.

About the Report

MetricsCart analyzed 7,567 protein powder products across 17 brands and 1,232 sellers on Google Shopping on 20 April, 2026. We also reviewed customer feedback collected from 384 sources, including bareperformancenutrition.com, 1upnutrition.com, transparentlabs.com, iherb.com, gnc.com, walmart.com, and other retail and brand sites.

This protein powder consumer report uses Google Shopping to show how the category is performing across visibility, sentiment, discounting, and purchase channels. The result is a clear picture of how protein powder brands are competing in 2026 and what shoppers are responding to.

Introduction

The protein powder market is no longer limited to gyms, bodybuilding communities, or specialty nutrition stores. In 2026, protein supplements have become a mainstream wellness category driven by fitness enthusiasts, busy professionals, athletes, weight-management consumers, and even quick-commerce shoppers ordering supplements alongside groceries.

The global protein powder market is surging to $19 billion in 2025, projected to double by 2035 as high-protein diets become mainstream. 61% of Americans increased their protein intake by 2024. Online retail leads distribution with a 38% share, driven by convenience and D2C growth, while traditional channels remain relevant.

Within this booming category, e-commerce is playing an outsized role: a recent industry report notes that protein powder distribution is heavily concentrated online, underscoring the need for strong digital retail strategies.

As brands jockey for shelf space and clicks, consumers are actively searching for the best protein powder 2026, weighing factors like price, reviews, and convenience.

This protein powder consumer report by MetricsCart uses digital shelf analytics software to compare brands across pricing, promotions, and consumer sentiment.

How RNWY and Bare Performance Nutrition Dominate Google Shopping Visibility

According to MetricsCart research findings, RNWY and Bare Performance Nutrition lead all brands by sheer assortment size on Google Shopping. RNWY lists 1,505 products (≈20% of category SKUs), and Bare Performance Nutrition lists 1,342 (18%).

This head start in volume translates directly into visibility: more listings mean more chances to appear for diverse search terms. In fact, Google’s shopping algorithms favor stores with broad catalogs and high inventory levels, so top-line coverage often means top-of-page exposure.

Together, RNWY and Bare Perf. Nutrition accounts for nearly 40% of all protein powder listings on Google Shopping, making them the de facto default brands in search results.

Why Listing Volume Matters in Protein Powder Discovery

Having hundreds of SKUs is more than just a numbers game. Each product listing comes with its own title, keywords, and ad potential. Brands with larger catalogs effectively “own” more search real estate.

For example, RNWY’s 1,505 listings span everything from whey isolates to pre-workouts, allowing them to capture niche and generic protein powder queries alike. By contrast, a smaller brand with only a few SKUs might only trigger a handful of search terms.

More listings also mean more Buy Box opportunities: with many variations available, RNWY and Bare Performance can optimize price and availability to dominate the Buy Box on a majority of their products. In short, greater listing volume equates to broader digital shelf presence and a higher chance of intercepting consumer searches early.

Mid-Tier Visibility: Transparent Labs and GNC

Transparent Labs and GNC represent a strong second tier, each with roughly 700 products on Google Shopping. These brands benefit from solid brand recognition and a moderately broad product range.

- Transparent Labs, known for science-backed formulations, targets fitness enthusiasts and maintains premium positioning.

- GNC, a retail giant, leverages its name recognition online despite fewer SKUs than RNWY/BPN.

Both brands focus on visibility in core segments (whey, casein, etc.), and their substantial but not overwhelming catalog size allows them to remain focused on top-selling items. They may not have RNWY’s sheer breadth, but their listings are concentrated on tried-and-true products, which can help maintain higher average ratings and tighter inventory control.

Brands Struggling for Shelf Presence

At the bottom end are brands like Build Fast Formula and Bal Bharat, each with only a handful of Google Shopping listings. These minimal catalogs indicate very limited market reach or an early-stage market test.

For these brands, poor visibility stems from low listing volume: they appear in few search results. Often, these niche companies rely on other channels (direct-to-consumer websites, specialized retailers) for sales.

Their low presence on Google Shopping suggests an opportunity gap: either expand the SKU range or improve feed optimization to increase discoverability. If their products are high quality, increasing presence on Google Shopping could unlock new demand.

Premium vs. Budget Protein Powder Strategies on Google Shopping

The insights from MetricsCart’s price monitoring software reveal that brands fall into two clear pricing camps. On the premium end, ATP Lab leads with an average price of $67.75 per unit, followed by GNC ($63.31) and Bal Bharat ($62.09). Transparent Labs ($58–61) and RAW Nutrition ($58–61) also sit in this upper tier.

These companies clearly target the high-end segment, emphasizing quality ingredients (e.g., grass-fed whey, unique formulations) and leveraging brand reputations. Premium positioning allows them to achieve higher margins and less reliance on discounts; as seen below, GNC and BAL Bharat offer minimal promotions.

By contrast, budget-oriented brands compete primarily on price. PhD Nutrition’s line averages just $27.72 per product which is roughly half the cost of the premium tier. Rule One Proteins is similar at $29.16. Even Bare Performance Nutrition, despite its large catalog, averages only $38.50.

These brands emphasize value: reasonable protein content at a low price.MetricsCart insights show that affordable price points, combined with large catalogs (like BPN), yield a high search presence.

Cheap pricing attracts the “best budget protein powder with best reviews” buyers: indeed, the brands listed above maintain strong overall ratings and high review volumes, proving that they can satisfy mass-market consumers even at lower price tiers.

Why ATP Lab Commands Premium Pricing

ATP Lab has intentionally curated a luxury image. They offer premium blends (often featuring niche ingredients such as egg white protein or specialty hydrolysates) and market to dedicated athletes. On Google Shopping, every ATP Lab product carries a hefty price tag (~$68 on average).

Customers who pay these prices expect top performance and purity. In turn, ATP Lab invests less in promotions (we observe only modest discounts on their listings).

This strategy seems sustainable: the brand’s presence, while smaller than RNWY’s, is highly visible among high-end keywords (e.g., “organic whey isolate”). This suggests ATP Lab knows its audience values perceived quality. Companies aiming to command such pricing should ensure their listings emphasize certifications and unique benefits to justify the premium.

Affordable Growth Strategy of PhD Nutrition

At the opposite end of the spectrum, PhD Nutrition is the standout budget leader. By pricing most of their products under $30, they attract price-sensitive shoppers.

What’s notable is that despite the low price, PhD maintains exceptional customer sentiment (around 87% positive reviews, the highest among major brands). This indicates a successful value proposition: customers feel they’re getting good quality for the price.

PhD’s growth strategy likely involves funneling those initial low-price buyers into brand loyalty. By undercutting competitors on price (while still delivering agreeable products), PhD captures market share in high-volume categories such as whey and casein.

For emerging brands aiming to compete, the lesson is that competitive pricing can win shelf space and reviews, especially if product quality is solid.

How Bare Performance Nutrition Balances Scale and Affordability

Bare Performance Nutrition (BPN) hits a sweet spot between scale and value. With the second-largest product count (1,342 listings) and a moderate average price of $38.50, BPN offers one of the strongest value-for-money propositions.

This combination helps explain their broad appeal. They carry many products, yet their pricing undercuts most premium brands by a wide margin. Despite this affordability, BPN still achieves very high sentiment (86% positive reviews), indicating customers trust their products.

Essentially, BPN’s strategy is to be both ubiquitous and reasonably priced. This likely drives both high organic search visibility and high sales volume. The key lesson is that dominating Google Shopping doesn’t require the highest prices; abundant SKUs at mid-tier prices can capture a large audience segment that wants quality at a fair price.

Discount Wars: How Myprotein Uses Promotions to Drive Visibility

Myprotein is a textbook case of a high-discount strategy. MetricsCart pricing and promotion monitoring software identified that Myprotein offers the largest average discount (~20%) among all brands. This aligns with its reputation: the UK-based brand is known for frequent sales and promotions.

High discounting serves to lift Myprotein’s Google Shopping rankings. By temporarily lowering prices, Myprotein’s listings become the cheapest in the category for many queries, effectively winning more Buy Boxes and clicks. This is particularly effective for a value-oriented international brand trying to gain traction in competitive markets.

High-Discount vs Low-Discount Brand Strategies

Not all brands follow Myprotein’s playbook. Rule One Proteins also sees significant discounts (16.44% avg.), targeting aggressive growth through promotions. On the other hand, GNC and Axe & Sledge hardly discount at all.

These low-discount brands rely on their established reputation and wide retail reach. Their Google Shopping strategy seems to be: maintain consistent pricing and let brand equity drive sales.

The analysis reveals that while discounts can boost visibility, a brand with high trust (like GNC) can afford to compete on reliability and availability instead. Other premium-focused brands (like Transparent Labs) strike a middle ground with modest or occasional discounts.

Why Premium Brands Avoid Aggressive Promotions

Premium-positioned brands tend to minimize discounts to protect margins and brand image. For example, we see GNC averaging very small markdowns; Transparent Labs and RAW Nutrition similarly limit promotions.

The rationale is to avoid training customers to expect deals on high-end products. Instead, premium brands may offer value in other ways (e.g. loyalty points, bundles) without deeply cutting prices.

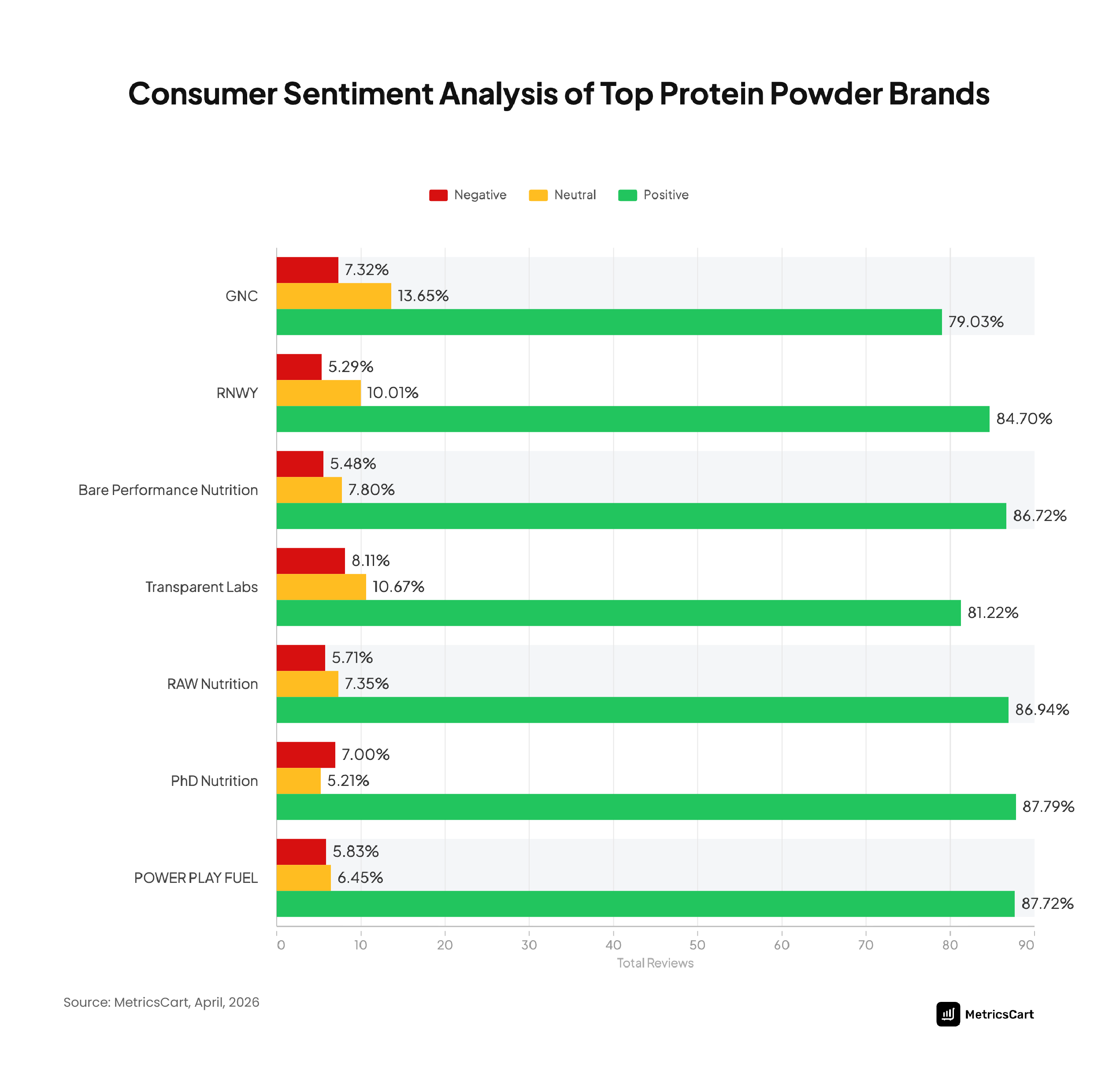

This strategy works if the products justify the cost: after all, Transparent Labs has one of the highest rates of negative feedback (8.11%), which may be partly due to disappointed, price-sensitive customers. By avoiding discounts, premium brands risk slower visibility growth, but they preserve a perception of exclusivity.

Customer Sentiment Trends Across Protein Powder Brands

Based on the MetricsCart consumer sentiment analysis of 195,000+ reviews, the category shows remarkably positive sentiment. Of 195,000 reviews, 158,051 are positive, 24,793 neutral, and only 12,092 negative.

In percentage terms, about 80% are positive, under 6% negative. This overwhelmingly positive feedback suggests that most protein powders sold meet or exceed consumer expectations.

In practice, this means very few products are outright flops. The implication for brands is that product quality in this category is generally high, so companies should focus on incremental improvements rather than addressing major complaints.

Why GNC Generates the Most Customer Engagement

GNC leads in total reviews with 36,332, slightly ahead of RNWY (34,784) and Bare Performance Nutrition (31,009). GNC’s dominance in engagement is unsurprising: it’s a long-standing chain with a huge customer base, and it leverages its retail recognition online.

In other words, many consumers already know GNC and leave reviews accordingly. However, quantity isn’t everything: among top brands, GNC’s positive rate is the lowest (79% positive, 13.7% neutral).

This could be because GNC’s massive sales volume includes a broader range of products, including lower-end lines, leading to more mixed feedback. Nonetheless, high engagement means GNC commands a top spot in conversations – a valuable asset.

High Positive Sentiment Leaders: PhD Nutrition and POWER PLAY FUEL

At the other end, PhD Nutrition and POWER PLAY FUEL have the highest positive review sentiment (~87–88%) among well-reviewed brands. PhD’s high satisfaction level (with 87% positive) is impressive given its budget positioning. It shows that budget-friendly products can still satisfy customers.

POWER PLAY FUEL, with similar positivity, suggests that even smaller niche brands (it has fewer total reviews than GNC) can achieve near-universal praise if they meet expectations. Bare Performance Nutrition and RAW Nutrition also exceed 86% positive.

These brands are clearly doing something right – perhaps strong flavor profiles, effective marketing, or reliable mixability – resulting in broad approval. High positivity can become a virtuous cycle: in Google Shopping, products with higher star ratings get more clicks, leading to more sales.

READ MORE | Consumer Sentiment Analysis for CPG Brands [2026 Growth Guide]

The Rise of Quick-Commerce Protein Shopping Through Uber Eats and Instacart

One of the most striking findings is the prominence of delivery platforms among top retailers. eBay is the largest source of protein powder buy box wins (378 listings), with Uber Eats (309 listings) and Instacart (252 listings) close behind.

Traditionally, nutrition products are sold through supplement sites or retailers; it is unusual to see meal delivery and grocery services so high in the rankings. This reflects a quick-commerce trend: on-demand platforms are expanding beyond food into everyday goods.

Uber’s quick commerce research notes that over 30% of orders now fall outside traditional food categories. Moreover, consumers appreciate the convenience: rather than going to the store, they can add a tub of whey to a quick grocery delivery.

The appeal is simple: immediacy and convenience. Busy shoppers who are already ordering groceries or meals may add protein powder or vitamins to a same-day basket. This is especially true during peak seasons (e.g., fitness resolutions) when people want products fast.

How Quick-Commerce Changes Supplement Discovery

The rise of quick-commerce channels changes the competitive landscape. Brands now have to optimize not just on Amazon and brand sites, but also on Uber Eats and Instacart storefronts. These platforms often emphasize local inventory and speed, so smaller retailers (even local supplement shops) can compete by offering immediate fulfillment.

This also means that optimization for Google may overlap with these delivery apps’ feeds. A brand needs to ensure its product appears at a local grocery (via Instacart) or convenience store (via Uber Eats) to capture on-demand traffic.

The Future of Nutrition Products in Instant Delivery

The trend towards instant delivery is likely to grow. Consumers increasingly expect not just food, but all their needs to be met quickly. Given that 86% of people now want same-day delivery for any item, nutrition brands should take note.

Being present on quick-commerce platforms can be a competitive differentiator. For brands with dense distribution, listing on Uber, Instacart, DoorDash, etc., may open a new revenue stream. It also means Google Shopping strategies must account for these channels, since Google may aggregate listings from any participating merchant.

In summary, quick-commerce is turning nutrition shopping into an impulse-friendly category, and brands that adapt will capture this growing demand.

READ MORE | 6 Reasons Why Brands Need Quick Commerce Tracker [Guide]

Why Most Protein Powder Listings Fail to Win the Buy Box

A key challenge is revealed by MetricsCart research: 91% of protein powder listings lack the Buy Box. Out of 7,567 products, only 694 have the Buy Box, meaning the vast majority (6,873 SKUs) never feature as the “Add to cart” default.

Similarly, only 21% of sellers (296 of 1,398) ever secure the Buy Box. In effect, roughly 4 out of 5 sellers are missing out on prime visibility and click-throughs.

The 91% Visibility Gap Across Protein Powder Products

Why do so many products fail to win the Buy Box? On Google Shopping, the Buy Box privilege goes to the seller with the best combination of price, stock, and ratings for each SKU. This means a single dominant seller can lock out all others.

Our analysis shows that for many protein powder listings, one seller consistently undercuts or outperforms competitors, winning the Buy Box repeatedly. All other sellers of that SKU are relegated to secondary listings, resulting in near-invisibility.

This “winner-takes-most” dynamic is common in well-optimized categories: our report on other categories shows that Buy Box control can skew heavily toward a few. For brands and sellers, the takeaway is that a Buy Box strategy is critical. Without it, even good products will languish with click-through rates 5x or more lower.

Seller Concentration and Competitive Advantage

The fact that only 296 sellers (21%) have ever won the Buy Box highlights extreme concentration. These winners are likely the largest retailers and most competitive players (think Walmart, Amazon channel partners, and the brands themselves).

Smaller sellers without the Buy Box essentially have no visibility unless a consumer specifically clicks through “More sellers” listings. This reinforces a vicious cycle: prominent sellers get more sales and reviews (improving their metrics), which keeps them in the Buy Box, whereas low-tier sellers get stuck.

It also means brand management on Google Shopping is critical: for brand owners and channel managers, it’s vital to monitor and, if possible, partner with those Buy Box sellers to ensure correct pricing.

How Pricing, Ratings, and Availability Influence Buy Box Wins

MetricsCart research underscores the importance of competitive pricing and high ratings. Most Buy Box winners on protein powders combine the lowest price with strong stock levels and high review scores.

Even a very cheap product can win if others are priced significantly higher. Conversely, products with identical prices often rely on higher review counts or faster shipping speeds. For example, the cheapest items primarily won the Buy Box through near-zero pricing.

On the other hand, some high-priced products still hold the Buy Box either because they are the only immediate option or because they have stellar reviews. The lesson: every brand should strive to optimize price, maintain inventory, and encourage positive reviews to vie for the Buy Box.

The Cheapest and Most Expensive Protein Powders Winning the Buy Box

What Low-Cost Buy Box Winners Reveal About Sampling Strategies

MetricsCart’s buy box monitoring solution identifies the absolute cheapest protein items that secure the Buy Box. These typically include single-serve samples or mini-packs, suggesting a deliberate sampling strategy.

| Products | Price |

| Rule One R1 Free Sample | $1.39 |

| The All New ATP Fuel Pro | $2.53 |

| ATP Recovery Pro Mix | $2.66 |

| BA HIGH PROTEIN MEAL REPLACEMENT – STRAWBERRY (single serving) | $3 |

| So Lean & So Clean Organic Protein Powder2 | $3 |

These rock-bottom prices indicate that some sellers use loss-leaders to attract customers. By placing a small product in the Buy Box, a seller gets clicks and traffic and can then upsell larger items or other brands in the basket.

It also shows that Google’s algorithm still allows ultra-low-priced SKUs to dominate the Buy Box, even if revenue is minimal. For marketers, these examples highlight an effective tactic: offering inexpensive trial-size products can generate new buyers, build reviews, and funnel them to full-size purchases later.

Why High-Priced Protein Products Still Convert

Surprisingly, some of the highest-priced protein powders also maintain the Buy Box. The top expensive Buy Box winners are:

| Products | Price |

| Whey Protein Isolate – Chocolate | $1100.70 |

| Collagen | $972 |

| BulkSupplements Hydrolyzed Whey Protein Isolate Powder | $299.97 |

| GNC Pro Performance Power Protein| Double Rich Chocolate | 4 Lbs & 100% Micellar Casein | | 25G Protein | 15G EAA | 7G BCAA | Chocolate Supreme | 2 | $266.31 |

| SAVAS Soy Protein 100 Cocoa Flavor [2000g] | $247.45 |

These products succeed despite (or because of) their high prices for a few reasons. Often, they are specialty or wholesale-size items, appealing to hardcore users or commercial buyers. For example, a 15 kg bulk whey isolate can be priced well over $1,000; its buyer pool is small but willing to pay for huge volume.

The GNC bundle and SAVAS soy powder cater to committed athletes who trust those brands and need specialized formulations. The fact that these expensive SKUs still win the Buy Box implies very low competition in those niches, often only one seller or the brand itself offers them.

It also suggests that a high price is not a barrier if value is perceived (bulk pricing per gram, brand trust, or specialty use).

Extreme Pricing and Premium Consumer Psychology

The dual existence of ultra-cheap and ultra-expensive Buy Box winners speaks to varied consumer mindsets. Some buyers are lured by sampling offers and bargains, while others want premium, high-investment products.

This segmentation is normal in protein marketing: entry-level users may try samples before committing, whereas experts may invest heavily. For brands, the insight is that there’s room at both ends of the spectrum.

Offering entry-level price points (even at cost) can drive volume and introduce customers to the brand. Simultaneously, maintaining premium, high-margin SKUs caters to a different segment and can be profitable per sale.

Understanding this price psychology helps brands tailor their assortment: don’t ignore the $1.39 visitor if you also offer the $1000 enthusiast.

What Protein Powder Brands Should Learn From MetricsCart Google Shopping Insights

This analysis reveals several lessons for supplement brands leveraging Google Shopping and quick-commerce channels:

Pricing Lessons for Emerging Brands

- Offer a clear value proposition. PhD Nutrition’s success shows that aggressive pricing can win market share and positive reviews. New brands entering the market should consider undercutting incumbents to climb into the Buy Box. However, quality must meet expectations, or negative reviews will offset gains.

- Use promotions strategically. Myprotein’s discount-driven visibility shows that time-limited sales can significantly boost exposure. Brands looking to accelerate growth may use coupons and deals during peak demand periods (e.g., New Year fitness season). However, premium brands should be cautious: cutting prices too often can damage perceived value.

- Monitor competitor pricing. With MetricsCart, brands can monitor rivals’ price changes in real time on Google Shopping. For example, if a competitor like Rule One drops their R1 sample to $1.39, your automated alerts can trigger a temporary matching price to prevent losing search share.

Review Strategy Insights for Premium Supplements

- Encourage feedback on high-end lines. Transparent Labs has one of the highest negative rates. Actively soliciting customer reviews and addressing criticisms (improving flavors, transparency) could help. Brands should view every review as an opportunity to refine their product or messaging.

- Leverage social proof. We see that brands with strong review counts (GNC, RNWY, BPN) also drive visibility. Premium brands should ensure their top sellers accumulate reviews quickly. Consider promotions that incentivize reviews (e.g., samples for influencers, reviewer rewards).

- Highlight top-rated SKUs. Google Shopping allows banners or badges for best sellers and high-rated products. Pinpoint your best-reviewed whey proteins (for example, any 4.9★ isolates) and feature them. Customers searching for “best whey protein powder reviews” will be drawn to highly rated listings.

Why Seller Optimization Matters More Than Ever

- Win the Buy Box by any means. Our findings show that ~79% of sellers are stuck without the Buy Box. Brands should ensure they (or their official retailers) are the ones winning it. This means competitive pricing, fast shipping, and high seller ratings. Even if you’re selling through third-party retailers, you should support them in meeting Buy Box criteria.

- Expand your seller footprint. The top sellers on Google Shopping are often not from a single retailer. Having multiple reputable resellers (with approved pricing) can increase the number of Buy Box opportunities. MetricsCart insights suggest that seller diversity can mitigate Buy Box risk if one seller falters.

- Own your brand presence. If possible, be your own seller on Google Shopping (Brand Storefront, etc.). That way, you directly control pricing and can appear in the Buy Box as the “authorized” seller, rather than letting others compete.

The Growing Importance of Multi-Platform Visibility

- Follow the customer across apps. With eBay, Uber Eats, and Instacart rising in the rankings, brands cannot ignore any channel where their product appears. Ensure your products are listed (or syndicated) on these platforms.

- Optimize for quick commerce. Since on-demand platforms often rely on proximity and inventory freshness, ensure your key SKUs are available in major metro areas through partnerships. This may involve working with retail chains or specialized quick-delivery services in your region.

- Use cross-channel analytics. Tools like MetricsCart can track Google Shopping performance and monitor listings on delivery apps (often via partnerships). By seeing which channel drives the most sales for a given SKU, brands can allocate inventory and marketing spend more efficiently.

By tracking competitor moves and consumer feedback, companies can continuously adapt. For example, MetricsCart alerts could notify a brand when a rival drops a price or a quick-commerce app starts carrying their products.

Armed with such insights, supplement brands can iterate faster, secure the Buy Box more often, and ultimately capture a larger share of the booming protein market. The metrics are clear: visibility + value + verified reviews = market leadership in online protein sales.

Ready to improve your protein powder brand’s visibility on Google Shopping?